SOC 2 Certification in Austin

CertPro is a Licensed CPA Firm conducting SOC 2 audit engagements for service organizations in Austin, Texas. All examinations are performed against the AICPA Trust Services Criteria, covering Security, Availability, Confidentiality, Processing Integrity, and Privacy. SOC 2 attestation scope is defined per organization and delivered as a formal Type I or Type II report under SSAE 18 professional standards.

OUR CLIENTS

Introduction to SOC 2 Certification in Austin

SOC 2 Certification in Austin represents a formal attestation issued by a licensed CPA firm confirming that a service organization’s controls meet the AICPA’s Trust Services Criteria (TSC). The framework was developed by the American Institute of Certified Public Accountants (AICPA) to provide independent assurance over how organizations manage customer data across five trust categories: Security, Availability, Processing Integrity, Confidentiality, and Privacy. For Austin-based service organizations, SOC 2 attestation serves as the standard mechanism for communicating control effectiveness to enterprise customers, business partners, and regulators.

SOC 2 compliance is not a pass-or-fail certification in the traditional sense. It is an examination conducted under the AICPA’s Statement on Standards for Attestation Engagements No. 18 (SSAE 18), which produces a formal opinion letter and a detailed report. The report describes the service organization’s system, lists the applicable trust services criteria, and provides the CPA firm’s conclusions regarding whether controls were suitably designed and — in the case of Type II reports — whether they operated effectively over a defined review period. SOC 2 Certification in Austin is widely demanded by enterprise clients who require documented evidence of vendor security practices before onboarding.

Austin has emerged as one of the most concentrated technology ecosystems in the United States. The city hosts major technology campuses operated by Dell Technologies, Apple, Google, Amazon, and IBM. Additionally, Austin’s fintech corridor and SaaS startup ecosystem — including companies clustered around the Domain, East Riverside, and the Central Business District — have created intense demand for SOC 2 audit documentation. Prospective enterprise clients routinely include SOC 2 report requests in vendor security questionnaires, procurement checklists, and contract negotiations. SOC 2 Certification in Austin is therefore not merely a security best practice but a commercial prerequisite for many B2B relationships in the region.

What Is SOC 2 and How Does It Differ from Other Frameworks

SOC 2 is a service organization control framework governed exclusively by the AICPA. It differs from ISO 27001 in both structure and purpose. ISO 27001 is a management system standard that results in a certificate issued by an accredited certification body. SOC 2, by contrast, produces an attestation report issued by a licensed CPA firm under professional audit standards. The SOC 2 report includes a detailed system description, management’s assertion, the CPA’s opinion, and — for Type II reports — a full description of tests performed and results obtained. This level of transparency is particularly valued by enterprise procurement teams because it provides substantive evidence rather than a summary certificate.

SOC 2 also differs from SOC 1, which addresses controls relevant to user entities’ financial reporting. SOC 2 examinations focus specifically on the security and operational integrity of a service organization’s systems as they relate to customer data handling. For Austin companies providing SaaS platforms, cloud infrastructure, data analytics, managed IT services, or payment processing, SOC 2 is the applicable report type. SOC 1 applies primarily to organizations whose systems affect downstream financial statement accuracy, such as payroll processors or transfer agents.

| Attribute | SOC 2 | ISO 27001 |

|---|---|---|

| Governing Body | AICPA | ISO/IEC |

| Output | Attestation Report | Certificate |

| Issuer | Licensed CPA Firm | Accredited Certification Body |

| Market Focus | U.S.-centric (widely accepted globally) | Global recognition |

| Detail Level | Tests specific controls per TSC and service commitments | Assesses management system conformance |

Trust Services Criteria: The Foundation of SOC 2 Compliance

The Trust Services Criteria (TSC) form the evaluative backbone of every SOC 2 engagement. The Security category — also called the Common Criteria — is mandatory in all SOC 2 examinations. It addresses logical and physical access controls, system operations, change management, and risk mitigation. The remaining four categories — Availability, Processing Integrity, Confidentiality, and Privacy — are optional and selected based on the nature of services provided and commitments made to customers. Austin service organizations operating mission-critical platforms or handling regulated data frequently include Availability and Confidentiality in their SOC 2 compliance scope.

The Privacy category within SOC 2 compliance aligns with the AICPA’s Generally Accepted Privacy Principles (GAPP). It addresses notice, choice and consent, collection, use and retention, access, disclosure to third parties, security for privacy, quality, and monitoring. Austin organizations subject to Texas data privacy obligations — including the Texas Data Privacy and Security Act (TDPSA), effective July 2024 — may find that incorporating the Privacy TSC into their SOC 2 scope provides a structured mechanism for demonstrating compliance with state privacy obligations alongside federal contract requirements.

SOC 2 Type I vs. Type II: Understanding the Distinction

SOC 2 Type I and Type II reports serve different purposes and carry different levels of assurance. A Type I report evaluates whether controls were suitably designed as of a specific point in time. It answers whether the controls management describes in the system description are actually in place and logically capable of meeting the relevant trust services criteria. A Type II report covers a defined examination period — typically six to twelve months — and evaluates both design suitability and operational effectiveness. The Type II opinion is based on testing performed across the full review period, examining whether controls functioned consistently and as intended throughout.

Enterprise customers in Austin’s technology sector almost universally request SOC 2 Type II reports because they demonstrate sustained control performance over time — not just a point-in-time snapshot. As noted in AICPA guidance, consistent control operation across months requires systematic processes, trained personnel, and documented evidence. Austin companies entering enterprise sales cycles should plan to complete a Type II audit to satisfy procurement requirements from larger customers, particularly those in financial services, healthcare, and government contracting sectors. SOC2 Certification at the Type II level delivers the most commercially recognized form of SOC 2 attestation available.

Why SOC 2 Reports Matter for Austin Businesses

Austin’s technology and financial services landscape creates specific commercial conditions in which SOC 2 reports function as essential business documents. The city hosts more than 9,000 technology companies, with the Austin metro area accounting for the third-largest concentration of technology employment in the United States. Organizations operating in this environment — whether providing SaaS platforms to enterprise clients, managing cloud infrastructure for regulated industries, or delivering data analytics to financial institutions — encounter SOC 2 report requests as a routine element of vendor due diligence. SOC 2 compliance Austin companies achieve through a licensed CPA firm examination enables access to commercial opportunities that would otherwise be foreclosed by vendor security requirements.

The Austin fintech ecosystem — including payment processors, lending platforms, insurtech providers, and digital banking infrastructure companies — operates under heightened scrutiny from institutional clients. Banks and financial institutions subject to OCC guidance, FFIEC examination standards, and state banking commission oversight require vendors who handle financial data to provide independent assurance documentation. SOC 2 Certification in Austin that fintech companies obtain satisfies these requirements and enables engagement with regulated financial institutions as a credible, audited vendor. Without a current SOC 2 report, many fintech service providers are categorically excluded from enterprise vendor panels at large financial institutions.

SOC 2 and Austin’s SaaS and Cloud Services Sector

SOC 2 compliance that Austin SaaS companies pursue has become a standard expectation in enterprise software procurement. Buyers across healthcare, legal, financial services, and government contracting segments issue vendor security questionnaires that include direct requests for SOC 2 Type II reports as a precondition to contract execution. Austin SaaS providers who complete SOC 2 attestation report shorter sales cycles with enterprise prospects, as documented security assurance reduces the due diligence burden on buyer security teams. Companies with current SOC 2 reports can direct procurement security reviews to the report rather than completing extensive questionnaire responses from scratch for every new prospect.

Austin’s cloud infrastructure providers — including those operating colocation facilities and managed service providers serving the Hill Country data center corridor — face similar demands. Customers co-locating equipment or purchasing managed services require assurance that physical security controls, environmental monitoring, access management, and change control processes meet documented standards. A SOC 2 audit that Austin data center and managed service operators undergo provides this assurance through independent examination and formal reporting, rather than through self-attestation or marketing claims.

SOC 2 in the Context of Texas Regulatory Requirements

Texas state law creates specific obligations for organizations handling personal data. The Texas Data Privacy and Security Act (TDPSA), effective July 1, 2024, applies to businesses that process personal data of Texas residents and meet defined threshold criteria. While TDPSA does not explicitly require SOC 2 Certification in Austin, the control categories evaluated in a SOC 2 examination — particularly the Security and Privacy trust services criteria — directly correspond to the technical and organizational measures TDPSA requires for data protection. Austin organizations subject to TDPSA that complete SOC 2 attestation create documented evidence of their data protection practices, supporting regulatory accountability obligations.

Texas state agencies and political subdivisions that contract with technology vendors may impose security requirements aligned with Texas Administrative Code Chapter 202, which governs information security for state agencies. Service providers to Texas government entities — including Austin-based companies serving state agencies, the University of Texas System, or Travis County — may face SOC 2 report requests as part of vendor security assessments. SOC 2 audit firms in Austin, Texas that qualify to conduct these examinations must hold CPA firm licensure and meet AICPA peer review program standards, ensuring that issued reports carry professional credibility recognized by government procurement officials.

Customer Trust and Competitive Differentiation in Austin Markets

SOC 2 Certification in Austin delivers measurable competitive differentiation in markets where multiple vendors offer comparable technical capabilities. When enterprise procurement teams evaluate competing vendors, the presence or absence of a current SOC 2 Type II report frequently determines which vendors advance past initial security screening. Austin technology startups that obtain SOC 2 attestation before entering enterprise sales cycles position themselves alongside established vendors who have completed the same independent examination process — reducing buyer hesitation related to vendor maturity and security practice documentation.

- ✓Satisfies enterprise vendor security questionnaire requirements with a formal audit report

- ✓Accelerates procurement approval processes by providing documented control evidence

- ✓Demonstrates SOC 2 compliance with AICPA Trust Services Criteria to regulated industry customers

- ✓Supports contract negotiations with financial institutions, healthcare organizations, and government agencies

- ✓Provides independent SOC 2 attestation that reduces buyer reliance on self-reported security claims

- ✓Enables participation in enterprise vendor panels that require current SOC 2 documentation

- ✓Strengthens the organization’s internal control environment through examination preparation

- ✓Creates a foundation for maintaining ongoing SOC 2 compliance through annual audit cycles

- ✓Supports Texas data privacy compliance obligations under TDPSA for applicable organizations

- ✓Positions Austin technology companies competitively against vendors without independent audit documentation

SOC 2 Examinations by a Licensed CPA Firm in Austin

SOC 2 examinations must be conducted by a licensed CPA firm registered under the AICPA peer review program. This requirement is not procedural formality — it ensures that the examining firm operates under enforceable professional standards, including independence requirements, quality control standards, and peer review oversight. These safeguards give report recipients confidence in the examination’s objectivity. CertPro performs SOC 2 audit engagements as a licensed CPA firm in full compliance with SSAE 18 and AICPA professional standards. The firm’s role is strictly limited to independent examination and reporting; management of the service organization retains responsibility for system design and control operation.

The independence requirement for SOC 2 examinations is governed by the AICPA’s Code of Professional Conduct. The examining CPA firm must be independent of the service organization in both fact and appearance — meaning it cannot have financial interests in, employment relationships with, or other impairments that would affect its objectivity. This professional independence is what distinguishes a SOC 2 attestation from internal assessments, vendor self-certifications, or non-CPA security assessments. Recipients of SOC 2 reports — including enterprise customers, regulators, and business partners — rely on this independence when making decisions based on the report’s conclusions.

AICPA Standards Governing SOC 2 Engagements

SOC 2 engagements are conducted under SSAE 18, specifically AT-C Section 205 (Examination Engagements), as applied through the AICPA’s Guide: Reporting on Controls at a Service Organization Relevant to Security, Availability, Processing Integrity, Confidentiality, or Privacy. This guide provides detailed implementation guidance for applying the Trust Services Criteria, structuring the system description, performing control testing, and issuing the examination report. The AICPA updates these standards periodically, and licensed CPA firms conducting SOC 2 audit engagements are required to apply current standards and guidance at all times.

The SOC 2 examination report includes five core components: a management assertion letter in which the service organization’s management asserts that the system description is fairly presented and controls were suitably designed (and operated effectively for Type II); the service auditor’s report containing the examination opinion; the system description prepared by management; the description of the trust services criteria and related controls; and, for Type II reports, the results of the service auditor’s tests of controls. This structured format allows report recipients to review both the organization’s representations and the independent auditor’s findings within a single document.

CertPro’s Examination Methodology

CertPro conducts SOC 2 audit engagements through a structured, evidence-based methodology aligned with AICPA standards. The examination process involves defining the scope and applicable trust services criteria, reviewing management’s system description for completeness and accuracy, evaluating control design against the relevant criteria, and — for Type II engagements — executing a testing program that covers the full examination period. Evidence reviewed during testing includes system-generated logs, access control records, change management documentation, incident reports, vendor contracts, configuration screenshots, and personnel records, among other categories specific to the defined scope.

CertPro’s examination approach treats each engagement as organization-specific. The testing program is tailored to the service organization’s system architecture, the applicable trust services criteria, the nature of services provided, and any subservice organizations whose functions are relevant to the defined scope. Austin organizations with complex multi-cloud architectures, hybrid infrastructure environments, or significant third-party dependencies receive examination programs that reflect those specific characteristics — not generic checklists. This specificity is required under AICPA standards and ensures that the resulting SOC 2 report accurately represents the organization’s actual control environment.

SOC 2 Engagement Scope in Austin

Defining the correct scope is one of the most consequential decisions in a SOC 2 engagement. Scope determines which systems, processes, personnel, and physical locations fall within the examination, which trust services criteria apply, and which subservice organizations must be addressed. For Austin service organizations, scope definition requires careful analysis of the services provided to customers, the systems used to deliver those services, the data processed and stored, and the contractual and regulatory obligations that govern service delivery. A scope that is too narrow may fail to satisfy customer requirements; a scope that is overly broad increases examination complexity and cost without proportionate benefit.

The system description — a required component of the SOC 2 report prepared by management — must describe the principal service commitments and system requirements, the components of the system (infrastructure, software, people, processes, and data), and the relevant aspects of the control environment. Austin organizations that operate multiple product lines or serve multiple customer segments should carefully evaluate whether a single SOC 2 engagement adequately covers all relevant services, or whether separate engagements are warranted for different system boundaries. CertPro works with each organization’s management to evaluate these questions during scope determination, which precedes formal examination procedures.

Selecting Applicable Trust Services Criteria

The Security category (Common Criteria) is mandatory in all SOC 2 examinations and forms the baseline evaluation framework. Organizations must evaluate whether additional trust services criteria categories should be included based on customer commitments, contractual obligations, and the nature of services delivered. Austin SaaS providers with service level agreement (SLA) commitments around uptime and availability should include the Availability TSC. Organizations processing transactions — such as payment processors or data transformation services — should consider the Processing Integrity TSC. Companies that contractually commit to keeping customer data separate from other clients’ data should include the Confidentiality TSC to satisfy SOC 2 compliance requirements fully.

The Privacy TSC applies to organizations that collect, use, retain, disclose, and dispose of personal information as part of their services. Austin companies subject to HIPAA, TDPSA, CCPA (for California residents), or other privacy frameworks may find that including the Privacy TSC in their SOC 2 scope provides a comprehensive mechanism for demonstrating compliance with multiple privacy obligations through a single examination. The Privacy TSC criteria align with the AICPA’s privacy framework and provide structured evaluation points across the full data lifecycle — from collection through disposal.

Subservice Organizations and Carve-Out vs. Inclusive Method

Austin service organizations frequently rely on cloud infrastructure providers — such as Amazon Web Services, Microsoft Azure, or Google Cloud Platform — whose controls are relevant to the service organization’s ability to meet trust services criteria. These entities are called subservice organizations, and their treatment in the SOC 2 scope requires a deliberate decision between the carve-out method and the inclusive method. Under the carve-out method, the SOC 2 report describes functions performed by subservice organizations but excludes their controls from the examination scope. Under the inclusive method, the subservice organization’s controls are included in the examination scope and tested directly.

Most Austin organizations using major cloud providers apply the carve-out method, referencing the cloud provider’s own SOC 2 reports — publicly available for AWS, Azure, and GCP — as supplementary evidence. This approach is accepted under AICPA standards as long as the service organization’s report clearly identifies the carved-out subservice organizations and the functions they perform. Organizations using smaller or less-known subservice organizations that lack their own SOC 2 reports may need to consider alternative approaches, including contractual security requirements, right-to-audit provisions, or other mechanisms to address subservice organization controls within the SOC 2 audit scope.

Requirements for SOC 2 Certification

SOC 2 Certification in Austin requires that a service organization meet specific documentation, technical, and organizational requirements sufficient to support a licensed CPA firm’s examination. These requirements are not defined by a fixed checklist but by the applicable Trust Services Criteria, which specify the control objectives and points of focus against which controls are evaluated. The AICPA’s 2017 Trust Services Criteria document — updated periodically with implementation guidance — provides the complete set of criteria applicable to SOC 2 examinations. Understanding these requirements in detail allows Austin organizations to structure their control environments appropriately before engaging a CPA firm for examination.

SOC 2 documentation requirements encompass policies, procedures, system descriptions, control evidence, and management assertions. The system description is a formal document prepared by management that describes the service organization’s system in sufficient detail to allow report recipients to understand the system boundaries, the components involved, and the controls in place. Policies must address the security and operational domains covered by the applicable trust services criteria — including information security, access management, change management, incident response, and vendor management — at minimum for organizations pursuing Security TSC coverage under SOC 2 compliance standards.

Procedures documentation must demonstrate how policies are implemented in practice. For SOC 2 Type II examinations, procedures must be documented before the start of the examination period — not created retroactively. Austin organizations undergoing a SOC 2 audit for the first time frequently discover gaps between documented policies and actual operational procedures during the examination process. The CPA firm’s role is to test whether documented controls operated as described, not to assist in creating or correcting documentation. Management retains full responsibility for ensuring that documentation accurately reflects the control environment before the examination period begins.

Technical control requirements for SOC 2 compliance address the logical and physical safeguards that protect system components and data. Under the Security TSC Common Criteria, organizations must demonstrate controls over logical access — including user provisioning, access reviews, multi-factor authentication for privileged and remote access, and termination procedures. System operations controls must address monitoring of system components, malware detection, vulnerability management, and backup and recovery procedures. Change management controls must demonstrate that changes to infrastructure, software, and configurations follow a defined process that includes authorization, testing, and documentation before implementation.

Physical security controls are also evaluated under the Security TSC for organizations that operate physical infrastructure or maintain on-premises systems. Data centers and server rooms must have controlled access with authentication mechanisms, visitor logs, and environmental monitoring. Austin organizations that rely entirely on cloud infrastructure may have fewer physical security controls to demonstrate directly, but they must address how physical security at co-located or cloud facilities is monitored and managed — typically through reference to the cloud provider’s SOC 2 reports and contractual security requirements. Encryption requirements — both in transit and at rest — are evaluated as part of the Security TSC and must be documented and tested during the SOC 2 audit.

Organizational requirements for SOC 2 compliance address the people, governance structures, and accountability mechanisms that support control operation. The Common Criteria include requirements related to the control environment — specifically management’s philosophy and operating style, organizational structure, assignment of authority and responsibility, and human resources practices. Background screening for employees with access to sensitive systems, security awareness training programs, and defined roles and responsibilities for security-relevant functions must all be documented and demonstrable through evidence reviewed during the SOC 2 examination.

Risk assessment is a specific Common Criteria requirement that mandates organizations identify, analyze, and respond to risks that could prevent the achievement of service commitments and system requirements. The risk assessment process must be documented, periodically updated, and linked to the controls in place to address identified risks. Austin organizations in high-growth phases frequently face challenges in maintaining formal risk assessment processes as their technical environments and customer bases evolve rapidly. The SOC 2 examination evaluates whether risk assessment processes are systematic and documented — not simply whether management believes risks have been considered informally.

- ✓Formal information security policy approved by management and communicated to all personnel

- ✓Documented user access provisioning and deprovisioning procedures with authorization controls

- ✓Multi-factor authentication implemented for remote access and privileged system access

- ✓Periodic access review processes with documented evidence of review completion

- ✓Vulnerability management program with defined scanning frequency and remediation timelines

- ✓Change management process with documented authorization, testing, and approval workflows

- ✓Incident response policy and procedure with defined detection, escalation, and resolution steps

- ✓Vendor management program addressing third-party security requirements and ongoing monitoring

- ✓Documented risk assessment process updated at defined intervals

- ✓Security awareness training program with records of employee completion

- ✓Documentation Requirements

- ✓Technical Control Requirements

- ✓Organizational and Personnel Requirements

How SOC 2 Examinations Work in Austin

The SOC 2 examination process follows a defined sequence of professional procedures governed by AICPA standards. Each stage has specific objectives, evidence requirements, and professional obligations for the examining CPA firm. Understanding how the examination works allows Austin service organizations to plan effectively, allocate internal resources appropriately, and ensure that management’s responsibilities are fulfilled throughout the engagement. The examination is not a one-time event — for Type II engagements, it spans a defined period during which controls must operate consistently and evidence must be contemporaneously generated and retained.

Stage 1: Scope Definition and Engagement Planning

The examination begins with formal scope definition, during which the service organization and the licensed CPA firm establish the boundaries of the system under examination, the applicable trust services criteria, the report type (Type I or Type II), and the examination period dates. For Type II engagements, the review period typically runs six to twelve months, though initial engagements may use shorter periods. The engagement letter formalizes these parameters and specifies the responsibilities of each party. Management is responsible for the system description, assertion, and control operation; the CPA firm is responsible for independent examination and reporting in accordance with AICPA standards governing SOC 2 attestation.

During the planning stage, CertPro reviews the service organization’s system description for completeness and accuracy relative to the defined scope. The system description must address all five components of a system — infrastructure, software, people, processes, and data — and describe how these components interact to deliver the in-scope services. Any identified gaps or inaccuracies must be addressed by management before the description is finalized, as it forms the basis for the examination and becomes part of the issued report. Austin organizations new to SOC 2 attestation frequently require multiple rounds of system description review to achieve the level of specificity required under AICPA standards.

Stage 2: Control Design Evaluation

Control design evaluation assesses whether the controls identified in the system description are logically capable of meeting the applicable trust services criteria. This evaluation applies to both Type I and Type II engagements. The CPA firm reviews control descriptions, interviews personnel responsible for control operation, and evaluates whether the design of each control addresses the relevant criteria point of focus. A control may be well-implemented technically but inadequately designed if it fails to address all relevant criteria aspects — for example, an access review control covering production systems but excluding development environments with access to customer data may have a design gap flagged during the SOC 2 audit.

Design evaluation findings that identify controls as not suitably designed result in exceptions noted in the examination report. For Type I engagements, design exceptions are the primary finding category. For Type II engagements, design exceptions may be identified if the CPA firm determines during the examination period that controls were not designed to meet the criteria — even if those controls appear to have been operating. Austin organizations should ensure that all controls mapped to the applicable trust services criteria have been reviewed for design adequacy before the formal examination period begins, as management retains responsibility for control design under AICPA professional standards.

Stage 3: Type II Control Testing and Evidence Review

Type II control testing is the most substantive component of a SOC 2 Type II examination. During this stage, the CPA firm executes a testing program that samples control operation across the examination period to assess whether controls functioned consistently and as described. Testing procedures may include inquiry, observation, inspection of documentation, and reperformance. Sample sizes are determined based on the nature and frequency of the control — automated controls that execute on every transaction may require smaller samples than manual controls performed monthly or quarterly. The AICPA’s practice guide provides direction on appropriate sampling approaches for different control categories within the SOC 2 audit framework.

Evidence reviewed during SOC 2 audit testing includes system logs, access control matrices, change tickets, incident records, training completion records, background check results, vendor contracts, configuration settings, and other documentation that demonstrates control operation. Austin organizations undergoing SOC 2 Type II examinations must maintain contemporaneous evidence throughout the examination period — evidence fabricated or reconstructed after the fact is not acceptable under professional standards and may result in examination findings or scope limitations. Evidence collection disciplines must be established before the examination period begins, not after the CPA firm requests samples.

Stage 4: Findings, Exceptions, and Report Issuance

Upon completion of testing procedures, the CPA firm evaluates findings and determines the examination opinion. Examination opinions may be unqualified (no exceptions noted), qualified (exceptions identified that do not affect the overall conclusion for other criteria), or adverse (pervasive exceptions that undermine the overall opinion). The majority of SOC 2 reports issued contain some exceptions — a single deviation in testing results in a noted exception but does not automatically result in a qualified opinion. The significance and pervasiveness of exceptions determine their impact on the overall SOC 2 attestation opinion.

The final SOC 2 report is a formal attestation document issued under the CPA firm’s professional authority. It is typically distributed on a restricted-use basis — the report is intended for the service organization, its customers, and potential customers who have agreements to receive it, not for general public distribution. Austin organizations should review distribution obligations carefully when sharing SOC 2 reports with prospects, customers, or regulators, as unauthorized distribution may raise questions about report confidentiality. CertPro’s issued reports include standard distribution restrictions consistent with AICPA guidance and applicable professional standards.

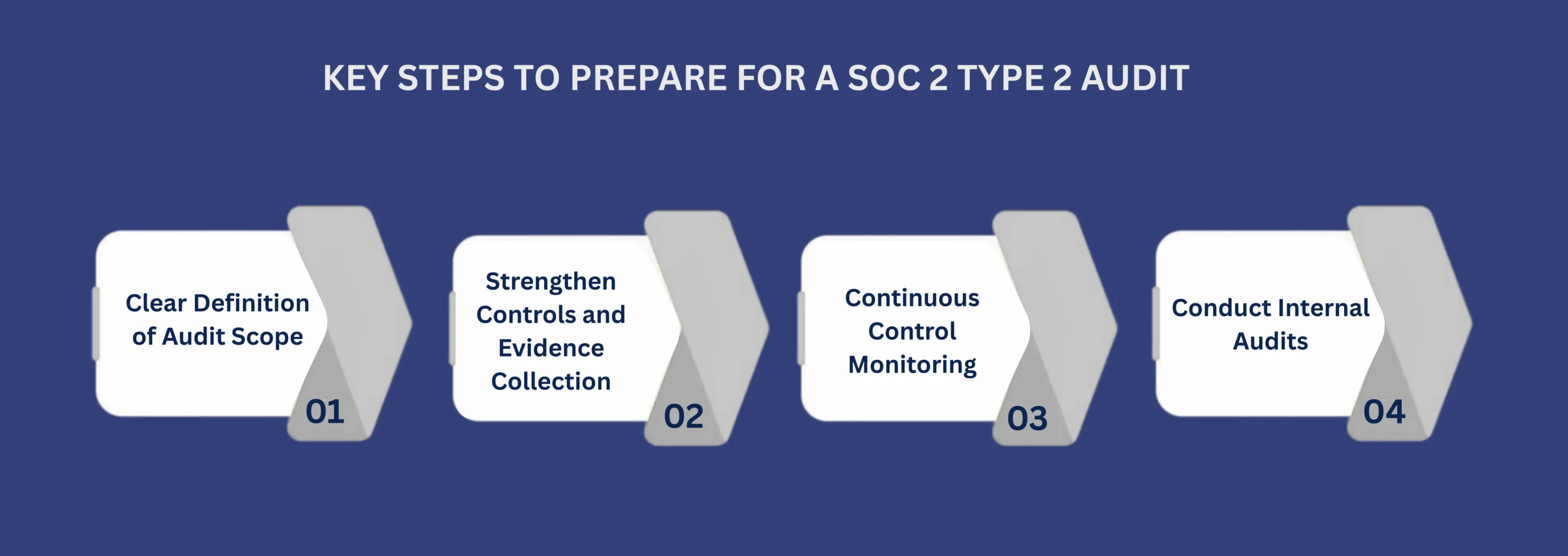

Steps for Obtaining SOC 2 Certification in Austin

Obtaining SOC 2 Certification in Austin follows a structured sequence of management and examination activities. Each step has defined responsibilities and produces specific outputs that feed into subsequent stages. Austin service organizations planning their first SOC 2 engagement should understand this sequence to allocate internal resources, establish realistic timelines, and ensure that management’s obligations are fulfilled before and during the examination. The process described below reflects the standard engagement structure for CertPro’s SOC 2 audit engagements conducted under AICPA standards.

- Determine the report type required (Type I or Type II) based on customer requirements and organizational objectives

- Define the system scope including in-scope services, infrastructure, personnel roles, and data categories

- Select applicable Trust Services Criteria based on service commitments and contractual obligations

- Prepare the system description document that accurately reflects the in-scope system and controls

- Identify and document all controls mapped to the applicable Trust Services Criteria points of focus

- Establish evidence collection processes to capture control operation documentation throughout the examination period

- Engage CertPro as the licensed CPA firm and execute the engagement letter formalizing scope and terms

- Complete the examination period with consistent control operation and contemporaneous evidence retention

- Support CertPro’s SOC 2 audit procedures by providing requested evidence, facilitating walkthroughs, and addressing questions

- Review the draft examination report, including management’s assertion, and finalize the SOC 2 attestation report for issuance

The timeline for completing SOC 2 Certification in Austin varies based on the report type and the organization’s control maturity. A Type I report — which assesses controls at a point in time — can typically be completed within six to twelve weeks from the start of examination procedures, assuming the system description is complete and controls are fully implemented. A Type II report requires the completion of the examination period (typically six to twelve months), plus the time required for testing procedures and report issuance — generally two to three additional months. Austin organizations with active enterprise sales cycles should plan SOC 2 audit timelines in coordination with anticipated customer requirements to ensure reports are available when needed.

Effective evidence collection is fundamental to a successful SOC 2 audit. Evidence must be contemporaneous — generated at the time of control operation — and specific enough to demonstrate that the control operated as described. Generic policy documents are not sufficient as evidence of control operation; specific records showing when, how, and by whom controls were executed are required. For access review controls, evidence includes actual review records showing which accounts were reviewed, by whom, on what date, and what actions were taken as a result. For vulnerability management, evidence includes scan reports, vulnerability findings, and documented remediation actions with completion dates.

Austin organizations frequently use GRC (Governance, Risk, and Compliance) platforms or security information management tools to automate evidence collection and organization. These tools can generate audit-ready evidence packages by capturing system logs, access records, and control performance data in structured formats. While tool-generated evidence can significantly improve efficiency in supporting a SOC 2 audit, it must still be reviewed for completeness and accuracy by management before being provided to the examining CPA firm. The CPA firm evaluates evidence independently and is not obligated to accept tool-generated data at face value without independent validation procedures.

- ✓Evidence Collection Strategy for SOC 2 Audits

SOC 2 Certification Cost in Austin

SOC 2 certification cost in Austin is determined by several factors, including the report type (Type I or Type II), the number of applicable trust services criteria, the complexity of the system under examination, the examination period length, and the number of controls requiring testing. CertPro determines engagement fees based on the defined scope and the audit procedures required under AICPA standards for each specific engagement. Fee structures reflect the professional time, expertise, and quality assurance requirements associated with producing a compliant SOC 2 attestation report that meets AICPA standards and withstands scrutiny by report recipients and the profession’s peer review program.

Type I examinations are generally less costly than Type II examinations because they assess controls at a point in time rather than over an extended period. Organizations pursuing their first SOC 2 report sometimes begin with a Type I examination to establish a baseline and then proceed to Type II in the following cycle. This approach allows management to confirm that the system description is accurate and controls are suitably designed before committing to the longer examination period required for Type II. However, organizations whose customers specifically require Type II reports should proceed directly to Type II rather than incurring the cost of two separate SOC 2 audit engagements.

Factors That Affect SOC 2 Examination Fees

System complexity is the most significant driver of SOC 2 examination fees. Organizations with large numbers of in-scope system components — multiple cloud environments, numerous application layers, complex data flows, or many personnel with system access — require more extensive testing programs than organizations with simpler, more uniform environments. The number of applicable trust services criteria also affects fees; adding Availability, Confidentiality, Processing Integrity, or Privacy to the Security baseline increases the criteria points of focus that must be addressed and the corresponding SOC 2 audit testing requirements. Austin technology companies with multi-product platforms or multi-tenant architectures should expect higher examination fees than single-product organizations with straightforward system boundaries.

| Cost Factor | Lower Cost Scenario | Higher Cost Scenario |

|---|---|---|

| Report Type | Type I (point-in-time) | Type II (12-month period) |

| Trust Services Criteria | Security only (Common Criteria) | Security + Availability + Confidentiality + Privacy |

| System Complexity | Single cloud environment, limited personnel | Multi-cloud, hybrid infrastructure, large teams |

| Examination Period | 6-month initial period | 12-month full annual cycle |

| Subservice Organizations | Major cloud providers with own SOC 2 reports | Multiple smaller subservice organizations without SOC 2 |

Annual recertification is a standard expectation for SOC 2 compliance that Austin organizations must plan for. Enterprise customers who receive SOC 2 reports expect annual renewals to maintain current assurance. A SOC 2 report covers only the examination period stated within it — a report covering January through December 2024 does not provide assurance about controls operating in 2025. Organizations that allow their SOC 2 reports to lapse may face customer audit requests, contract renegotiations, or removal from approved vendor panels. Annual engagement planning allows organizations to manage SOC 2 certification costs predictably and maintain continuous attestation coverage.

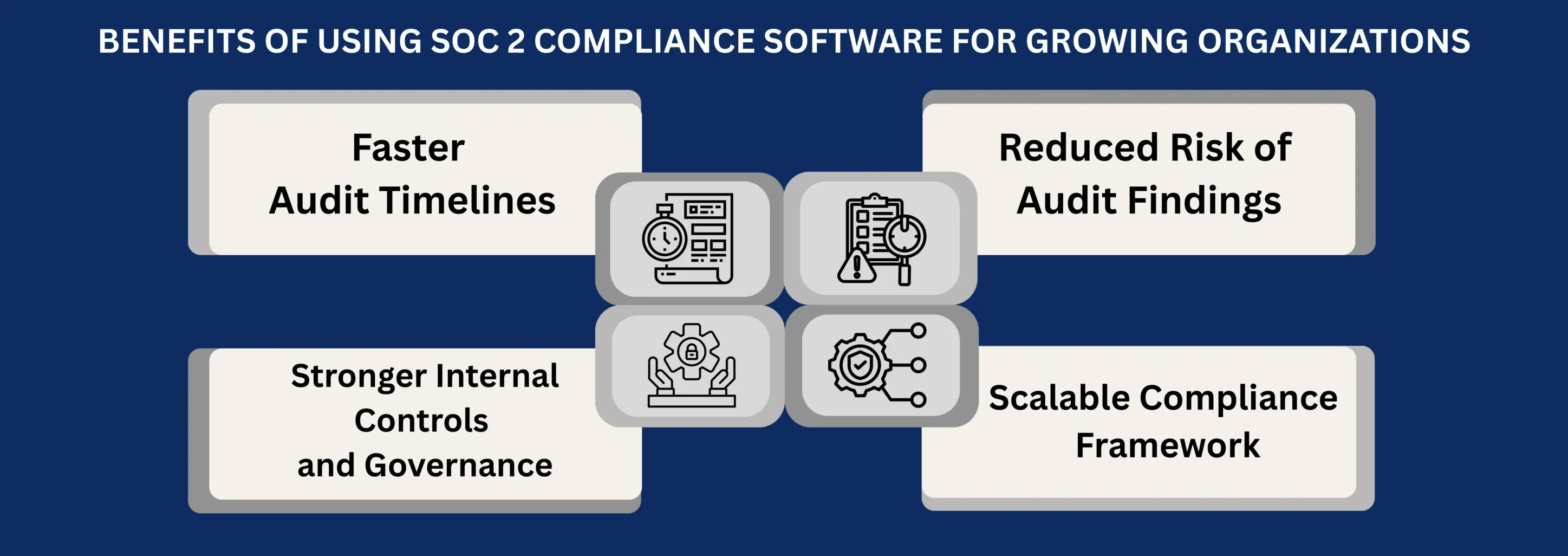

Benefits of SOC 2 Reports for Austin Businesses

A SOC 2 report provides independent, professionally credentialed assurance over how an organization’s systems and controls operate. For Austin businesses competing in the enterprise technology market, this assurance translates directly into commercial value. SOC 2 attestation enables engagement with customers who require documented vendor security evidence, supports contract negotiations with regulated industries, and demonstrates organizational maturity in data protection practices. Beyond commercial applications, the examination process itself surfaces control gaps and operational inconsistencies that — when addressed — strengthen the organization’s actual security posture, not just its documentation.

SOC 2 Certification in Austin delivers measurable impact on sales cycle efficiency for companies pursuing enterprise deals. Enterprise procurement processes for technology vendors typically include security review stages that can extend deal timelines by weeks or months. Organizations with current SOC 2 Type II reports can often satisfy security review requirements by sharing the report, directing buyer security teams to specific sections addressing their concerns, and providing supplementary information about exception items if present. This process is substantially faster than responding to lengthy vendor security questionnaires from scratch for each prospective customer.

SOC 2 Certification in Austin also supports fundraising and investor due diligence processes for tech startups. Venture capital and private equity investors conducting technical due diligence on security-sensitive technology companies increasingly request SOC 2 reports as evidence of operational maturity. A current SOC 2 Type II report demonstrates that the organization has established repeatable processes, maintains documented controls, and has submitted to independent professional examination — all of which reduce investor concerns about operational risk and scalability. For Austin startups entering growth-stage financing rounds, SOC 2 Certification provides evidence-based support for valuations premised on enterprise market penetration.

The operational benefits of SOC 2 compliance extend well beyond the report itself. The examination process requires organizations to formally document processes, establish consistent procedures, and implement monitoring mechanisms that many high-growth technology companies have not previously formalized. These improvements persist after the examination concludes and contribute to reduced operational risk, improved incident detection capabilities, and more consistent service delivery. Austin SaaS companies report that completing a SOC 2 audit reveals operational inconsistencies in areas such as access management, change control, and vendor oversight that — when remediated — improve service reliability and reduce security incident frequency.

Data breach preparedness is meaningfully strengthened through the control requirements associated with SOC 2 compliance. Organizations that maintain the incident response, access control, encryption, and monitoring controls required to meet the Security TSC are substantially better positioned to detect, contain, and respond to security incidents than organizations without formal control programs. The cost of a data breach — including regulatory penalties, customer notification obligations under Texas law, legal liability, and reputational damage — typically far exceeds the annual cost of maintaining SOC 2 Certification. Austin organizations that view SOC 2 compliance as a risk management investment rather than a compliance cost typically achieve better long-term return on their certification expenditure.

SOC 2 attestation simplifies third-party vendor risk management obligations for Austin organizations’ own customers. When a business provides services to organizations that are themselves subject to regulatory oversight — such as banks, healthcare providers, or government contractors — those organizations have obligations to assess and monitor vendor security. A current SOC 2 report issued by a licensed CPA firm satisfies many vendor risk management requirements, reducing the customer’s administrative burden and demonstrating that independent examination has already been performed. This benefit is particularly valuable for Austin service organizations serving multiple regulated-industry customers, as a single SOC 2 report can satisfy the vendor assessment requirements of dozens of customers simultaneously.

- ✓Commercial and Revenue Benefits

- ✓Operational and Security Benefits

- ✓Regulatory and Third-Party Relationship Benefits

Why Austin Businesses Engage CertPro for SOC 2 Examinations

Organizations seeking SOC 2 Certification in Austin engage CertPro because CertPro operates as a licensed CPA firm registered under the AICPA peer review program. This registration means CertPro’s SOC 2 examination practice is subject to independent quality review, ensuring that engagements are conducted in accordance with professional standards. SOC 2 reports issued by CPA firms subject to peer review carry the institutional credibility that enterprise customers, regulators, and business partners require when evaluating vendor security documentation. Reports issued by non-CPA firms or unregistered entities do not carry this professional credibility and are not recognized as valid SOC 2 attestations under AICPA standards.

CertPro’s SOC 2 audit engagements follow SSAE 18 standards with a focus on objective evaluation of controls against the applicable Trust Services Criteria. The firm applies professional judgment to scope determination, control testing design, evidence evaluation, and opinion formation. Each engagement is staffed by qualified professionals with experience in SOC 2 examination methodology, information systems auditing, and the technical domains relevant to the service organization’s system. Austin organizations in specialized technology sectors — including fintech, healthtech, legal technology, and government technology — receive examination teams with relevant domain familiarity to ensure technical controls are evaluated with appropriate depth.

CertPro’s Position as an Independent Examination Firm

CertPro’s role in SOC 2 engagements is strictly limited to independent examination and reporting. The firm does not provide implementation services, framework development, or operational security management — activities that would compromise the independence required under AICPA professional standards. This structural independence is essential to the credibility of SOC 2 reports issued under CertPro’s signature. Enterprises, financial institutions, and government agencies that receive CertPro’s SOC 2 attestation reports can rely on the objectivity of the examination conclusions because the issuing firm has no operational involvement in the service organization’s control environment.

Austin organizations evaluating CPA firms for SOC 2 examinations should confirm that the selected firm holds current CPA licensure, participates in the AICPA peer review program, maintains professional indemnity insurance appropriate to attestation engagements, and has documented experience with SOC 2 audit engagements under SSAE 18. CertPro satisfies all of these criteria and maintains the professional infrastructure required to issue SOC 2 reports recognized by enterprise customers as credible, standards-compliant attestations. SOC 2 audit firms that Austin, Texas organizations engage should be prepared to provide evidence of their peer review status upon request.

Engage CertPro for SOC 2 Examinations in Austin

CertPro performs SOC 2 audit engagements for service organizations in Austin, Texas as a licensed CPA firm operating under AICPA peer review program oversight. Engagements are scoped based on organizational characteristics, applicable trust services criteria, and defined examination period parameters. The resulting SOC 2 attestation report is issued under professional standards and carries the institutional credibility required by enterprise customers, financial institutions, healthcare organizations, and government agencies that request SOC 2 documentation from their vendors. SOC 2 Certification in Austin conducted by CertPro provides organizations with formally attested evidence of control design and operational effectiveness, delivered through a report that meets AICPA standards in every material respect.

Austin organizations at any stage of SOC 2 planning — including those evaluating whether Type I or Type II is appropriate, determining which trust services criteria apply, or assessing the scope of their system under examination — may contact CertPro to discuss engagement parameters. CertPro’s examination team evaluates each organization’s circumstances and provides scope and fee information based on the specific characteristics of the system and the applicable AICPA standards. SOC 2 audit engagements in Austin conducted by CertPro reflect the professional rigor required to produce reports that satisfy the scrutiny of enterprise security teams, regulated-industry compliance officers, and professional peer reviewers.

Austin’s technology economy continues to expand, and with it the commercial demand for independent security assurance documentation. SOC 2 attestation that Austin service organizations obtain through a licensed CPA firm examination is the recognized mechanism for meeting this demand. CertPro’s engagement approach is examination-focused, standards-compliant, and structured to produce formal SOC 2 attestation reports that accurately represent each organization’s control environment and examination results. Organizations committed to maintaining SOC 2 compliance that Austin enterprises require are encouraged to contact CertPro to initiate engagement planning and establish a timeline aligned with their customer requirements and business objectives.

FAQ

▶

What is the difference between SOC 2 certified and SOC 2 compliant?

▶

How long does a SOC 2 Type II examination take for an Austin organization?

▶

Which Trust Services Criteria should Austin SaaS companies include?

▶

Can small Austin startups afford SOC 2 certification?

▶

How does SOC 2 relate to HIPAA compliance for Austin healthtech companies?

▶

What happens if exceptions are found during a SOC 2 audit?

▶

Should Austin companies pursue SOC 2 or ISO 27001 first?

▶

How often must SOC 2 certification be renewed in Austin?

SOC 1 VS SOC 2: WHICH REPORT YOUR CUSTOMERS ACTUALLY ASK FOR

If you sell SaaS or provide outsourced services, you have likely been asked for a SOC report. However, the follow-up question is rarely easy to answer…

Secure Email Platform Exclaimer Renews ISO, SOC 2

Excerpt from The Manila Times Article, Published on February 26, 2026 Secure email solutions provider Exclaimer has renewed its ISO and SOC 2 certific…

SOC 2 FRAMEWORK REQUIREMENTS IN 2026. WHAT HAS CHANGED?

Security reviews used to happen at the tail end of a deal. Today, they happen in the first conversation. Enterprise buyers come prepared. They ask abo…

Get In Touch

have a question? let us get back to you.