SOC 2 Certification in Hong Kong

CertPro is a Licensed CPA Firm conducting SOC 2 audits for service organizations operating in Hong Kong. Engagements are structured against the AICPA Trust Services Criteria, covering Security, Availability, Confidentiality, Processing Integrity, and Privacy. Both Type I and Type II attestation reports are issued following independent control evaluation across defined audit periods.

OUR CLIENTS

Introduction to SOC 2 Certification in Hong Kong

SOC 2 Certification in Hong Kong represents a formal attestation framework developed by the American Institute of Certified Public Accountants (AICPA). It evaluates whether a service organization’s controls effectively meet the Trust Services Criteria (TSC). For organizations operating within Hong Kong’s technology-driven financial ecosystem, SOC 2 attestation serves as an independently verified declaration of data security posture, control design, and operational effectiveness.

SOC2 Certification is not a regulatory mandate in Hong Kong, but it functions as a de facto industry standard for service organizations managing sensitive customer data — particularly in cloud computing, fintech, SaaS, and data centre operations.

Hong Kong operates as one of Asia’s premier financial and technology hubs, hosting over 9,000 technology companies, major international banks, asset management firms, and a rapidly expanding fintech sector. This ecosystem is regulated by the Hong Kong Monetary Authority (HKMA) and the Securities and Futures Commission (SFC).

Within this environment, enterprise clients, institutional investors, and multinational corporations routinely require service providers to demonstrate SOC 2 compliance as a precondition for vendor onboarding. SOC 2 Certification in Hong Kong therefore represents both a competitive differentiator and a contractual necessity for organizations seeking to serve regulated industries.

What Is SOC 2 Certification?

SOC 2 certification is an attestation report issued by a Licensed CPA Firm following an independent audit of a service organization’s internal controls. These controls are evaluated against one or more of the five AICPA Trust Services Criteria: Security, Availability, Processing Integrity, Confidentiality, and Privacy.

The Security criterion — also referred to as the Common Criteria — is mandatory for all SOC 2 engagements. Organizations select additional criteria based on the nature of their services and the contractual commitments they make to customers.

SOC 2 differs from other certification frameworks such as ISO 27001 in its structure and output. While ISO 27001 results in a certificate of conformance against an international standard, SOC 2 produces an attestation report describing specific controls, test results, and auditor opinions. This report-based model gives enterprise clients granular visibility into a vendor’s control environment.

For Hong Kong organizations serving US-headquartered clients or entities listed on US exchanges, SOC 2 attestation remains the preferred compliance evidence format, making SOC2 Certification a strategic priority for internationally focused service providers.

SOC 2 Type I vs. SOC 2 Type II: Key Distinctions

SOC 2 Type I certification in Hong Kong evaluates the design and implementation of controls at a specific point in time. A Type I report confirms that controls were suitably designed as of a defined date, providing an initial attestation of control existence.

Organizations new to the SOC 2 audit process often pursue Type I as a first engagement. It establishes a documented baseline of control architecture and produces an attestation report that can be shared with prospective clients while a longer observation period accumulates toward a Type II engagement.

SOC 2 Type II certification in Hong Kong evaluates both the design and the operating effectiveness of controls over a defined observation period — typically six to twelve months. A Type II report provides substantially greater assurance because the Licensed CPA Firm tests whether controls operated consistently and effectively throughout the review window, not merely on a single date.

For organizations in Hong Kong’s financial services, cloud infrastructure, and managed IT sectors, Type II reports are the standard requested by enterprise clients and institutional counterparties. The observation period must be explicitly defined in the audit scope and agreed upon before engagement commencement.

| Attribute | SOC 2 Type I | SOC 2 Type II |

|---|---|---|

| Evaluation Focus | Control design at a point in time | Control design and operating effectiveness over a period |

| Audit Duration | Weeks to months | Six to twelve months observation period |

| Assurance Level | Design-level assurance | Design and operational assurance |

| Report Utility | Initial vendor qualification | Enterprise and institutional vendor requirements |

| Typical Use Case | Early-stage certification baseline | Ongoing annual compliance reporting |

The Five Trust Services Criteria Explained

The AICPA Trust Services Criteria form the evaluative foundation of every SOC 2 audit. The Security criterion requires that system resources are protected against unauthorized access, unauthorized disclosure, and damage to systems affecting availability, integrity, confidentiality, and privacy of information.

This criterion encompasses logical and physical access controls, change management procedures, risk assessment processes, incident response procedures, and monitoring activities. It is the only mandatory criterion and must be included in every SOC 2 engagement, regardless of the organization’s service type.

The Availability criterion evaluates whether systems are available for operation and use as committed or agreed. This is particularly relevant for Hong Kong data centre operators, cloud service providers, and managed service organizations where uptime commitments are contractually defined.

The Processing Integrity criterion applies where accuracy, completeness, and timeliness of transaction processing are fundamental — including payment processors and financial data platforms. Confidentiality addresses obligations to protect designated confidential information. Privacy governs the collection, use, retention, and disposal of personal information in alignment with applicable regulatory frameworks, including Hong Kong’s Personal Data (Privacy) Ordinance (PDPO).

Why SOC 2 Certification Matters for Hong Kong Organizations

Hong Kong’s position as Asia’s leading international financial centre creates a unique regulatory and commercial environment in which data security attestation carries measurable economic value. The city hosts regional headquarters of major global banks, insurance firms, asset managers, and technology companies subject to oversight from the HKMA, SFC, Insurance Authority (IA), and the Office of the Privacy Commissioner for Personal Data (PCPD).

These regulators and the institutional clients they supervise place increasing emphasis on third-party vendor security verification. As a result, SOC 2 compliance in Hong Kong has become a critical operational requirement for service organizations operating in the B2B space.

The HKMA’s Supervisory Policy Manual TM-G-1 on General Principles for Technology Risk Management — and its Circular on Strengthening Bank-wide Approach to Managing Third-Party Risk — explicitly require authorized institutions to conduct due diligence on outsourced service providers. SOC 2 attestation reports have become a standard evidence document submitted during vendor assessments by banks and financial institutions regulated under these frameworks.

Similarly, the SFC’s Guidelines for Reducing and Mitigating Hacking Risks reference independent security assessments as evidence of control adequacy. This further embeds SOC 2 compliance in Hong Kong into fintech and capital markets vendor requirements.

SOC 2 Compliance in Hong Kong’s Fintech Sector

SOC 2 compliance for Hong Kong fintech organizations is driven by multiple converging pressures. Hong Kong’s fintech ecosystem — which includes over 800 licensed and registered fintech firms as of 2024 — operates within a regulatory environment that increasingly treats data security posture as a licensing and partnership prerequisite.

Virtual asset service providers (VASPs) licensed under the Anti-Money Laundering and Counter-Terrorist Financing Ordinance, and operators of stored value facilities (SVFs) licensed by the HKMA, frequently receive requests for SOC 2 reports from international banking partners conducting third-party risk assessments.

Beyond regulatory-driven demand, fintech organizations in Hong Kong competing for enterprise contracts with multinational corporations headquartered in North America and Europe encounter SOC 2 audit requirements as a standard procurement condition. Enterprises subject to US Securities and Exchange Commission (SEC) oversight, or operating under contractual frameworks governed by US law, routinely insert SOC 2 Type II attestation requirements into service agreements.

For Hong Kong fintech firms targeting these markets, SOC 2 Certification in Hong Kong represents a direct enabler of revenue growth and partnership formation.

SOC 2 and Hong Kong’s Personal Data (Privacy) Ordinance

The Personal Data (Privacy) Ordinance (PDPO), administered by the Office of the Privacy Commissioner for Personal Data, governs the collection, holding, processing, and use of personal data in Hong Kong. While the PDPO and SOC 2 operate under different legal and professional frameworks, organizations pursuing the Privacy Trust Services Criterion will find that controls evaluated under that criterion align substantively with PDPO data protection principles.

These include purposes of collection, data accuracy, retention limits, security safeguards, and access rights — making SOC 2 compliance a complementary tool for organizations managing PDPO obligations.

The 2021 amendments to the PDPO introduced new provisions addressing doxxing and expanded the PCPD’s enforcement powers, including the authority to conduct compliance investigations and issue enforcement notices. Organizations that have obtained SOC 2 attestation covering the Privacy criterion demonstrate documented, independently tested privacy controls.

These controls can serve as evidence of due diligence during PCPD enforcement inquiries. This intersection makes SOC 2 compliance particularly relevant to data processors and cloud service providers operating under data processing agreements with Hong Kong-based data controllers.

Demand from Financial Services and Listed Companies

Hong Kong hosts numerous companies listed on the Hong Kong Stock Exchange (HKEX), including constituents of the Hang Seng Index and FTSE-tracked Hong Kong equities. Listed companies operating under the Corporate Governance Code and the Environmental, Social and Governance (ESG) Reporting Guide increasingly disclose third-party vendor risk management practices — including security attestation requirements imposed on IT and data service providers.

SOC 2 audit reports provide listed companies with documentary evidence supporting their own internal control disclosure obligations under these frameworks.

The insurance sector regulated by the Insurance Authority (IA) and pension management organizations operating Mandatory Provident Fund (MPF) schemes are similarly active consumers of SOC 2 attestation reports from technology vendors. The IA’s Guidelines on Cybersecurity reference independent audits and penetration testing as components of robust cybersecurity management programs.

This creates an environment where SOC 2 audit services in Hong Kong are directly relevant to insurance technology vendors serving this regulated market segment.

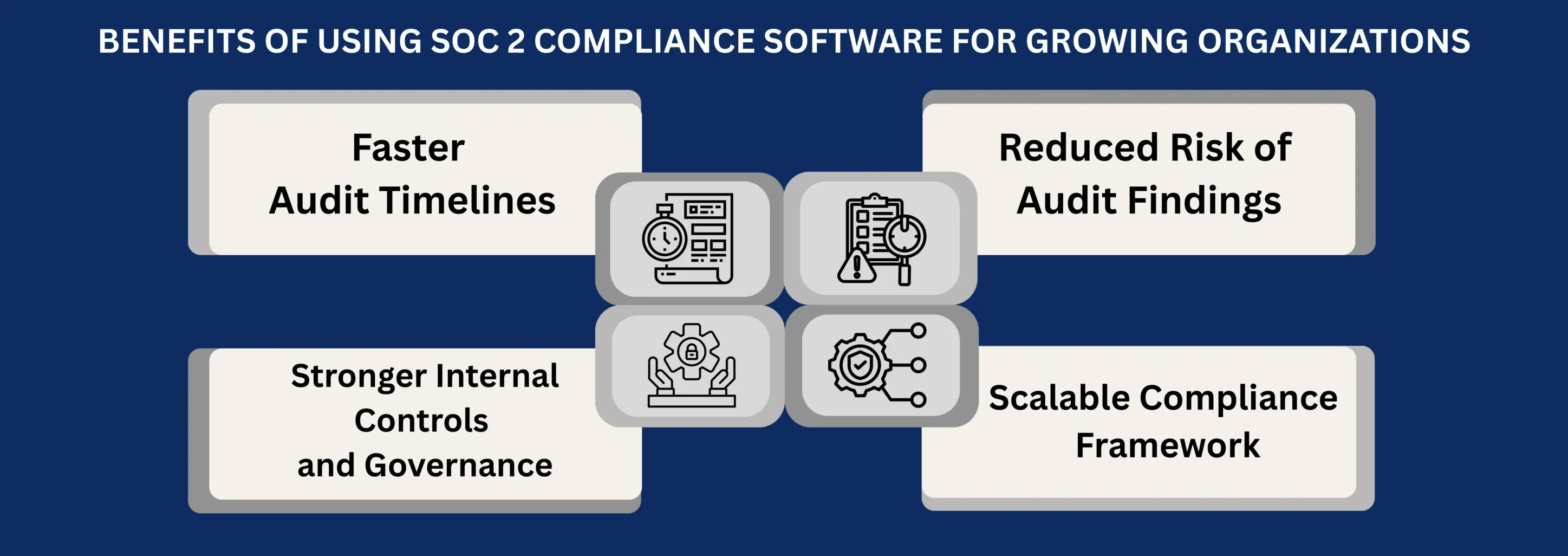

Benefits of SOC 2 Certification in Hong Kong

SOC 2 Certification in Hong Kong delivers measurable operational and commercial benefits to service organizations across multiple dimensions. The attestation report produced following a SOC 2 audit serves as an independently verified document that communicates the state of an organization’s control environment to customers, partners, investors, and regulators.

This transparency mechanism reduces friction in enterprise sales cycles, vendor due diligence processes, and regulatory examinations — providing a structured, auditor-reviewed evidence artifact without requiring access to internal systems or proprietary documentation.

- ✓Provides independently verified evidence of security control design and operating effectiveness to enterprise clients

- ✓Accelerates vendor qualification and procurement approval processes with regulated financial institutions

- ✓Demonstrates alignment with HKMA third-party risk management guidance for technology service providers

- ✓Supports PDPO compliance documentation through independently tested privacy controls

- ✓Strengthens the organization’s data incident response posture through structured control evaluation

- ✓Enables participation in US-linked commercial contracts requiring SOC 2 attestation as a contractual condition

- ✓Reduces customer security questionnaire burden by providing a referenceable, structured attestation report

- ✓Supports board-level governance reporting by providing an objective assessment of the control environment

- ✓Establishes a repeatable annual audit cycle that drives continuous control improvement

- ✓Differentiates service offerings in competitive Hong Kong cloud, SaaS, and managed IT markets

SOC 2 certification for Hong Kong companies directly expands serviceable market reach by satisfying the attestation requirements embedded in enterprise procurement frameworks. Major technology buyers, multinational corporations with Asia-Pacific regional headquarters in Hong Kong, and internationally operating banks with Group-level vendor management policies routinely exclude unattested vendors from approved supplier lists.

Achieving SOC 2 Type II certification removes this barrier and positions the certified organization as a qualified vendor in procurement pipelines that would otherwise be inaccessible.

In Hong Kong’s competitive SaaS and cloud infrastructure market, SOC 2 attestation functions as a quality signal that influences purchasing decisions beyond formal procurement requirements. Buyers conducting informal vendor evaluation often prioritize SOC 2-attested vendors over unattested competitors — even where the contract does not formally require attestation — because the report provides confidence in control maturity without requiring the buyer to conduct their own security assessment.

This dynamic is particularly pronounced in the financial services technology sector, where security risk management is a fiduciary concern and control evidence is expected at the outset of any commercial relationship.

The SOC 2 audit process requires organizations to maintain continuous, demonstrable evidence of control operation across the audit observation period. This evidence collection requirement — covering access reviews, change management logs, incident records, vendor assessments, and backup verification — creates structured operational discipline that extends well beyond the audit itself.

Organizations completing SOC 2 audit cycles develop systematic evidence management practices that improve the reliability and consistency of internal control operations across their entire service environment.

Centralized logging and monitoring systems implemented to satisfy SOC 2 evidence requirements — such as Security Information and Event Management (SIEM) platforms and log aggregation infrastructure — deliver ongoing operational security benefits. These include faster incident detection, improved forensic capability, and reduced mean time to containment during security events.

These investments serve a dual purpose: they satisfy SOC 2 audit evidence requirements while simultaneously strengthening the organization’s actual security posture in the Hong Kong threat landscape, where state-sponsored cyber activity and financially motivated attacks on financial sector infrastructure are persistent concerns.

SOC 2 compliance in Hong Kong supports alignment with multiple regulatory frameworks simultaneously. The HKMA’s Cybersecurity Fortification Initiative (CFI) 2.0 establishes a risk-based cybersecurity assessment framework for authorized institutions and their technology providers. Its control domains overlap significantly with SOC 2 Security Trust Services Criteria.

Organizations holding current SOC 2 Type II attestation reports can reference their audit findings during CFI assessments to demonstrate a control environment independently evaluated by a Licensed CPA Firm.

For venture-backed and private equity-owned organizations in Hong Kong, SOC 2 attestation increasingly features as a due diligence requirement in investment rounds and M&A transactions. Investors and acquiring entities conducting technology due diligence evaluate the target organization’s security posture as a component of enterprise value assessment and post-transaction integration risk.

An existing, current SOC 2 Type II attestation report provides investor due diligence teams with structured, auditor-reviewed evidence that reduces perceived technology risk and can positively influence transaction valuation and timeline.

- ✓Enhanced Market Access and Revenue Enablement

- ✓Operational Control Improvement Through Audit Evidence

- ✓Regulatory Alignment and Investor Confidence

SOC 2 Audit Process in Hong Kong

The SOC 2 audit process conducted by CertPro as a Licensed CPA Firm follows a structured engagement methodology aligned with AICPA AT-C Section 205 (Examination Engagements) and the Trust Services Criteria. Each stage is defined by specific evaluation activities, evidence requirements, and professional judgments.

The process is designed to produce an attestation report that accurately reflects the state of the organization’s control environment relative to the selected Trust Services Criteria and the defined audit scope.

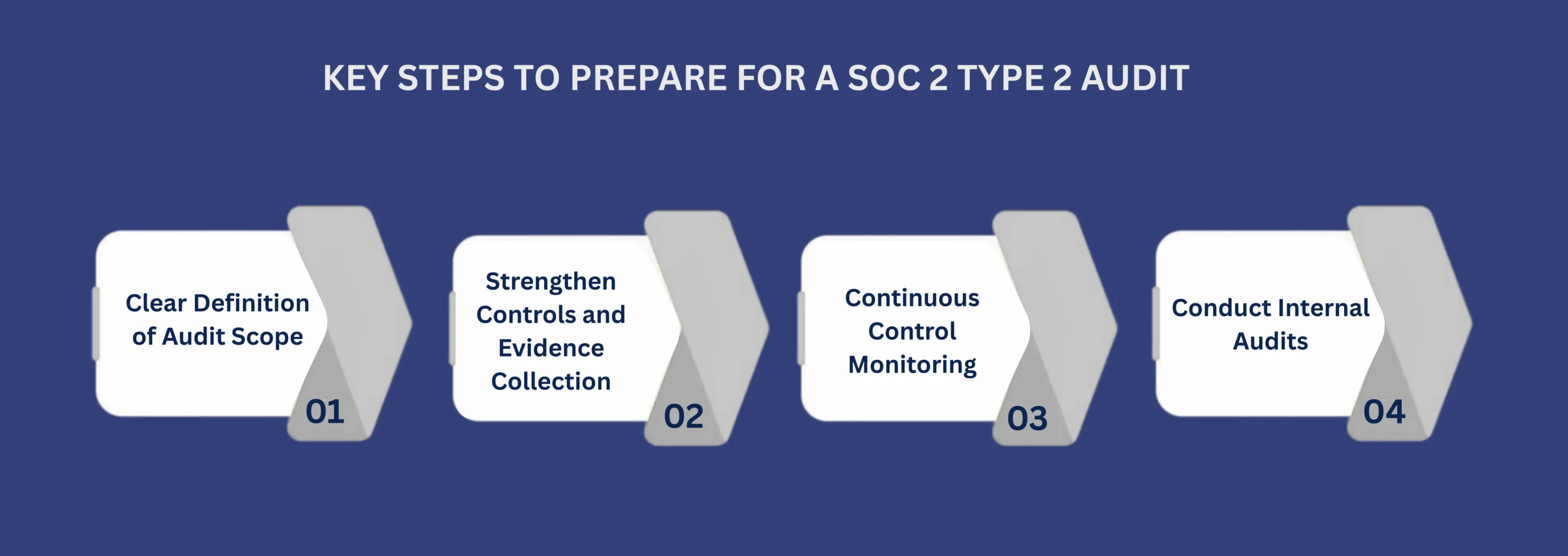

Scope definition is the foundational stage of the SOC 2 audit. The auditor and the service organization’s management jointly establish the boundaries of the system under examination. This includes identifying the infrastructure components, software applications, people, procedures, and data that together constitute the system relevant to the Trust Services Criteria being evaluated.

The system description — prepared by management and included in the final SOC 2 report — must accurately characterize the system and the controls in place to meet each criterion.

During scope definition for SOC 2 audit engagements in Hong Kong, the auditor determines which Trust Services Criteria apply based on the nature of the services provided and the commitments made to customers. For a Hong Kong cloud service provider, the Security and Availability criteria will typically be in scope. For a payment processing organization, Processing Integrity may be added. For an HR software vendor handling employee personal data, the Privacy criterion is relevant.

The scope documentation also identifies any subservice organizations — such as infrastructure providers like AWS or Google Cloud data centres operating in Hong Kong — and determines whether they are carved out or inclusive in the report.

Following scope confirmation, the Licensed CPA Firm develops a detailed audit program specifying the procedures to be performed for each Trust Services Criterion included in the engagement. The audit program identifies specific control objectives, the controls mapped to each objective, and the evidence types required to evaluate design adequacy and — for Type II engagements — operating effectiveness.

Evidence types include policy documentation, configuration screenshots, system-generated reports, personnel training records, access review logs, change management tickets, incident records, and vendor contract documentation.

For SOC 2 Type II engagements, the audit program includes a sampling methodology that determines how many instances of each recurring control will be tested over the observation period. Control testing frequency is determined by the nature of the control: automated daily controls may require a sample of 25 instances, while monthly management reviews may require testing all instances during the audit period.

The audit program is finalized before evidence collection begins and documents the professional basis for all subsequent testing activities.

The control design evaluation stage assesses whether the controls identified in the system description are suitably designed to meet the specified Trust Services Criteria. For a control to be suitably designed, it must be capable of achieving its stated objective when operating as designed, and no significant deficiencies should exist in the combination of controls addressing each criterion.

The auditor evaluates design through inquiry, observation, inspection of documentation, and walkthrough procedures that trace a transaction or process through the control environment.

SOC 2 Type I certification in Hong Kong is achieved at the conclusion of this stage, when the auditor issues an opinion on the fairness of management’s description and the suitability of control design as of the specified date. For organizations that have not previously completed a SOC 2 engagement, the Type I report serves as documented evidence that a structured control environment exists and has been independently evaluated.

This report can be shared with prospective clients while the Type II observation period accumulates toward a more comprehensive operating effectiveness attestation.

Operating effectiveness testing is the defining characteristic of SOC 2 Type II certification. During this stage, the auditor performs substantive testing of individual control instances across the observation period using the sampling methodology defined in the audit program. Testing procedures include inspection of evidence artifacts, re-performance of control procedures, corroborative inquiry with control operators, and analysis of system-generated records.

Each tested control instance is evaluated against the control description in the system description to determine whether the control operated as described and achieved its intended objective.

When deviations are identified during testing — instances where a control did not operate as described — the auditor evaluates the nature, cause, and frequency of the deviation to determine whether it represents a significant control deficiency. Deviations that are isolated and do not indicate systemic control failure may result in a qualified exception noted in the report without affecting the overall audit opinion.

Systemic or high-frequency deviations affecting one or more Trust Services Criteria may result in a qualified or adverse opinion on operating effectiveness for the affected criterion.

Following the completion of all testing procedures, the Licensed CPA Firm conducts a nonconformity review that consolidates all findings, evaluates their combined significance, and determines the appropriate audit opinion. Management is provided with a draft report for accuracy review, during which factual corrections to the system description may be made.

Management’s response to identified exceptions — including root cause analysis and corrective action plans — may be included in the final report to provide context to report users.

The final SOC 2 attestation report, issued by CertPro as the engaged Licensed CPA Firm, contains the service auditor’s report including the opinion, management’s assertion, the system description, and the detailed control testing results including any exceptions noted.

SOC 2 attestation reports issued in Hong Kong are distributed under restricted use provisions — typically shared with current and prospective customers, their auditors, and regulators — under a non-disclosure framework consistent with AICPA attestation standards.

SOC 2 compliance is not a one-time achievement. Organizations must complete annual audit cycles to maintain current certified status and meet customer expectations for up-to-date attestation. Industry practice and customer contractual requirements typically demand annual SOC 2 Type II reports covering a continuous 12-month observation period.

Gaps in attestation coverage — periods not covered by an active audit — are noted by sophisticated clients and may trigger additional due diligence requirements or contract compliance discussions.

Annual recertification cycles for SOC 2 Certification in Hong Kong should be planned to align with customer contract renewal schedules and regulatory examination cycles. Organizations serving HKMA-regulated institutions should ensure their Type II reports cover the 12-month period most likely to be requested during the bank’s annual third-party vendor review process.

Early engagement with the Licensed CPA Firm to plan the audit timeline ensures that observation periods are appropriately structured and that the final report is available when needed to satisfy contractual and regulatory evidence requirements.

- ✓Stage 1: Scope Definition and System Description

- ✓Stage 2: Audit Program Development and Evidence Planning

- ✓Stage 3: Control Design Evaluation (Type I Assessment)

- ✓Stage 4: Operating Effectiveness Testing (Type II Assessment)

- ✓Stage 5: Nonconformity Review, Certification Decision, and Report Issuance

- ✓Stage 6: Surveillance and Annual Recertification

Requirements for SOC 2 Certification in Hong Kong

Achieving SOC 2 Certification in Hong Kong requires organizations to satisfy both documentary and technical requirements across the Trust Services Criteria included in the audit scope. These requirements are not a prescriptive list of specific technologies or configurations. Rather, they represent a set of control objectives that must be demonstrably met through a combination of policies, procedures, technical safeguards, and operational practices.

The following sections detail the primary requirement categories that organizations must address prior to and throughout the SOC 2 audit engagement.

SOC 2 compliance requires organizations to maintain a comprehensive policy framework that formally documents the controls implemented to meet each Trust Services Criterion. Essential policy documents include an Information Security Policy, Acceptable Use Policy, Access Control Policy, Incident Response Policy and Plan, Business Continuity and Disaster Recovery Plan, Vendor Management Policy, Change Management Policy, and a Data Classification Policy.

Each policy must be formally approved by management, communicated to relevant personnel, and reviewed at defined intervals — typically annually — with evidence of review maintained throughout the SOC 2 audit period.

Beyond top-level policies, SOC 2 audit evidence requirements demand operational procedures that translate policy statements into specific, executable steps. These procedures cover user access provisioning and deprovisioning, change management approval workflows, vulnerability scanning and patch management, log review and alerting, and incident classification and escalation.

For SOC 2 Type II engagements, adherence to these procedures throughout the observation period must be evidenced through system records and activity logs that the auditor can inspect and test.

Technical controls form the operational backbone of a SOC 2-compliant environment. Access management controls must implement the principle of least privilege, requiring that users are granted only the access necessary to perform their job functions. Multi-factor authentication (MFA) must be enforced for remote access and privileged account access.

Role-based access control (RBAC) frameworks must be implemented across production systems, and access reviews must be performed on a defined periodic basis — typically quarterly — with documented evidence of each review cycle.

Encryption requirements under the Security criterion mandate that data in transit and data at rest be protected using industry-standard encryption protocols. TLS 1.2 or higher for data in transit and AES-256 for data at rest represent the current industry baseline for SOC 2 audit purposes.

Vulnerability management programs must include periodic internal and external vulnerability scanning, a defined remediation timeline for identified vulnerabilities categorized by severity, and evidence that critical and high-severity vulnerabilities are remediated within the timeframes established in the organization’s vulnerability management policy.

SOC 2 audit evaluation of organizational controls encompasses personnel security practices, security awareness training programs, and the assignment of defined roles and responsibilities for security and compliance functions. Background check procedures for personnel with access to sensitive systems and data must be documented and consistently applied.

Security awareness training must be delivered to all personnel at defined intervals — at minimum annually — and completion records must be maintained as audit evidence covering the full observation period for Type II engagements.

A designated individual or committee must hold formal accountability for information security governance within the organization. This organizational control requirement ensures that security decisions are made through a defined governance structure rather than informally.

Board or senior management oversight of information security risk — documented through meeting minutes or formal risk committee reporting — demonstrates the tone-at-the-top commitment to security that the AICPA Trust Services Criteria expect as an environmental control supporting all other criterion-level controls.

- ✓Formally approved and annually reviewed Information Security Policy

- ✓Documented Incident Response Plan with defined escalation procedures and evidence of testing

- ✓Access control framework implementing least privilege with periodic access reviews

- ✓Multi-factor authentication for remote and privileged access accounts

- ✓Encryption of data in transit (TLS 1.2+) and data at rest (AES-256 or equivalent)

- ✓Vulnerability scanning program with documented remediation timelines and evidence

- ✓Change management procedures with documented approval workflows and rollback plans

- ✓Security awareness training program with completion records for all personnel

- ✓Business Continuity and Disaster Recovery Plan with evidence of testing

- ✓Vendor management program with security assessment requirements for critical subservice organizations

- ✓Documentation and Policy Requirements

- ✓Technical Control Requirements

- ✓Organizational and Human Resources Requirements

SOC 2 Certification Cost in Hong Kong

The cost of SOC 2 Certification in Hong Kong varies based on several organizational factors — including the size and complexity of the systems in scope, the number of Trust Services Criteria included in the audit, the maturity of existing controls, and whether the engagement is a Type I or Type II assessment. There is no fixed regulatory fee for SOC 2 attestation; costs are determined by the scope of the Licensed CPA Firm’s engagement and the audit procedures required to produce the attestation report.

Factors That Influence SOC 2 Audit Costs

Organizational complexity is the primary cost driver for SOC 2 audit engagements in Hong Kong. A startup operating a single SaaS application hosted on a major cloud platform with a small team will have a significantly narrower audit scope than a mid-sized managed service provider operating multiple platforms, maintaining a hybrid cloud and on-premises environment, and employing hundreds of personnel across multiple Hong Kong offices.

The broader the system boundary and the greater the number of controls to be tested, the more audit procedures are required — and the higher the associated cost.

The number of Trust Services Criteria included in the audit scope directly affects cost because each additional criterion introduces new control domains requiring documentation, walkthrough, and testing procedures. Organizations including only the mandatory Security criterion will incur lower audit costs than those adding Availability, Confidentiality, Privacy, or Processing Integrity.

The decision regarding which criteria to include should be driven by customer contractual requirements, the nature of services provided, and the organization’s data handling commitments — not primarily by cost minimization.

| Cost Factor | Lower Cost Scenario | Higher Cost Scenario |

|---|---|---|

| Organization Size | Small team, single system | Large organization, multiple systems |

| Trust Services Criteria | Security only (1 criterion) | Security + 3-4 additional criteria |

| Report Type | SOC 2 Type I (point-in-time) | SOC 2 Type II (12-month observation) |

| Environment Complexity | Single cloud platform, no subservice orgs | Hybrid environment, multiple data centres |

| Control Maturity | Well-documented, consistently operated controls | Controls requiring remediation during audit |

Ongoing Investment in Annual Audit Cycles

The total investment in SOC 2 compliance in Hong Kong extends beyond the Licensed CPA Firm’s audit fee to include internal personnel time devoted to evidence collection, policy maintenance, control operation, and communication with the audit team. For organizations completing their first SOC 2 audit cycle, internal time investment is typically highest because documentation must be created, control owners must be identified, and evidence collection workflows must be established.

Subsequent annual cycles are generally more efficient because the documentation framework and evidence collection processes are already in place.

Technology investments in security tooling — SIEM platforms, identity and access management systems, vulnerability scanners, and configuration management databases — represent a significant component of the total SOC 2 compliance investment for organizations that do not already operate mature security infrastructure. However, these investments are not audit-specific costs; they are operational security expenditures that deliver ongoing security benefits independent of the audit cycle.

The SOC 2 audit engagement verifies that these tools are in place and operating effectively; it does not mandate specific commercial products.

SOC 2 Certified vs. SOC 2 Compliant: A Critical Distinction

A fundamental distinction exists between an organization that is SOC 2 certified and one that is SOC 2 compliant. SOC 2 compliance means that an organization has implemented internal controls that align with the Trust Services Criteria. SOC 2 certification — more precisely, SOC 2 attestation — means that a Licensed CPA Firm has independently evaluated those controls and issued a formal attestation report.

Compliance without attestation provides no externally verifiable evidence and cannot be shared with customers as an independent assessment of the control environment.

Organizations that describe themselves as ‘SOC 2 compliant’ without holding a current attestation report from a Licensed CPA Firm are making an unverified self-assessment claim. Enterprise clients, regulated financial institutions in Hong Kong, and US-headquartered buyers that have embedded SOC 2 requirements in their vendor contracts require the actual SOC 2 attestation report — not a self-declaration of compliance.

The distinction matters commercially and legally, because misrepresentation of certification status can constitute a breach of vendor representations in service agreements.

Why Independent Attestation Matters

The value of SOC 2 attestation derives directly from its independence. The Licensed CPA Firm conducting the SOC 2 audit has no financial or operational relationship with the service organization that would create a conflict of interest. The firm operates under AICPA professional standards that impose quality control requirements, continuing education obligations, and peer review processes.

This independence structure is what distinguishes an attestation report from a self-assessment and what gives customers, auditors, and regulators confidence in the report’s findings.

SOC 2 attestation reports in Hong Kong must be issued by a CPA firm licensed to perform attestation engagements. Not all cybersecurity firms, management consultants, or compliance software vendors are authorized to issue SOC 2 reports. Only Licensed CPA Firms with qualified attestation practitioners can produce the legally recognized attestation report that satisfies enterprise and regulatory requirements.

When evaluating SOC 2 service providers in Hong Kong, organizations should confirm the provider’s CPA licensing status and attestation practice credentials before engaging.

SOC 2 vs. ISO 27001: Choosing the Right Framework for Hong Kong

Hong Kong service organizations frequently evaluate whether to pursue SOC 2 Certification in Hong Kong, ISO 27001 certification, or both. The choice depends primarily on customer requirements and target markets. SOC 2 is the preferred framework for organizations serving US-headquartered enterprise clients, financial institutions operating under North American regulatory oversight, or any buyer that specifically requires a SOC 2 attestation report as a vendor qualification condition.

ISO 27001 is a globally recognized standard with broader international recognition — particularly in European, Middle Eastern, and Asia-Pacific markets outside the North American sphere.

The two frameworks differ in their output and evaluative focus. SOC 2 produces an attestation report that tests specific controls against defined Trust Services Criteria and documents test results with exceptions. ISO 27001 produces a certificate of conformance against the international standard’s requirements, validated through a certification audit but without the same level of control-specific testing evidence.

SOC 2 audit reports are therefore more detailed and provide more granular visibility into control operations, while ISO 27001 certificates are more universally recognized as a market access credential in non-North American markets.

| Dimension | SOC 2 | ISO 27001 |

|---|---|---|

| Output | Attestation report with control test results | Certificate of conformance |

| Geographic Recognition | Primarily North America, used globally | Global recognition across all markets |

| Evaluating Body | Licensed CPA Firm only | Accredited certification body |

| Detail Level | Tests specific controls against TSC | Evaluates ISMS against standard requirements |

| Renewal Cycle | Annual attestation reports | 3-year certification with annual surveillance |

When Both Frameworks Are Required

Organizations serving a global customer base from Hong Kong frequently hold both SOC 2 attestation and ISO 27001 certification simultaneously. The control frameworks overlap significantly in the areas of access management, risk assessment, incident management, and business continuity. This means investment in controls for one framework generates compliance evidence that is usable in the other.

Organizations that implement a unified control framework addressing both sets of requirements reduce duplication of effort and optimize the total compliance investment across both annual audit cycles.

The sequencing of framework adoption for Hong Kong organizations should be driven by customer requirements. If the primary client base includes US financial institutions and technology buyers, SOC 2 Certification in Hong Kong should be the first priority. If the organization is pursuing European Union market entry, ISO 27001 and consideration of GDPR-aligned privacy controls may take precedence.

Where both frameworks are ultimately required, a coordinated implementation approach that aligns evidence collection, audit timelines, and policy documentation across both programs produces the most efficient compliance posture.

Why Choose CertPro for SOC 2 Certification in Hong Kong

CertPro is a Licensed CPA Firm authorized to conduct SOC 2 attestation engagements for service organizations. The firm’s SOC 2 audit practice is staffed by qualified attestation practitioners with experience across Hong Kong’s financial services, technology, and data centre sectors. CertPro’s engagement methodology is structured to produce attestation reports that meet AICPA AT-C Section 205 requirements and satisfy the evidence standards expected by enterprise clients, regulated financial institutions, and institutional investors conducting vendor due diligence in the Hong Kong market.

CertPro conducts SOC 2 audit services in Hong Kong across all five Trust Services Criteria and issues both Type I and Type II attestation reports. The firm’s audit practitioners evaluate Security, Availability, Confidentiality, Processing Integrity, and Privacy controls using AICPA-aligned testing procedures designed to produce reliable, defensible attestation opinions.

Engagement timelines are structured to align with client business calendars, ensuring that completed reports are available to meet customer contractual deadlines and regulatory submission requirements.

Licensed CPA Firm Credentials and Professional Standards

As a Licensed CPA Firm, CertPro operates under the AICPA’s professional standards for attestation engagements, including quality control standards under SQCS No. 8 and independence requirements under the AICPA Code of Professional Conduct. These professional obligations ensure that every SOC 2 attestation report issued by CertPro reflects an independent, objective evaluation of the service organization’s control environment — free from conflicts of interest that could compromise the reliability of the auditor’s opinion.

CertPro’s attestation practitioners possess the technical security expertise required to evaluate the complex cloud and network control environments that characterize modern service organizations in Hong Kong. Evaluating controls such as network segmentation, encryption key management, identity federation, and containerized deployment environments requires technical knowledge that extends well beyond traditional financial audit skills.

CertPro’s audit teams combine CPA-licensed attestation authority with technical security evaluation capability to produce SOC 2 reports that accurately reflect the actual state of the organization’s control environment.

Sector-Specific Experience in Hong Kong Markets

CertPro has conducted SOC 2 audit engagements across Hong Kong’s key service organization sectors, including financial technology, cloud infrastructure, managed IT services, healthcare data management, and professional services platforms. This sector-specific experience enables the audit team to identify control considerations unique to each industry context.

This includes the intersection of SOC 2 compliance with HKMA regulatory requirements for fintech vendors, SFC cybersecurity guidelines for capital markets technology providers, and PCPD privacy enforcement considerations for personal data processors.

For organizations pursuing SOC 2 certification that Hong Kong financial services clients specifically require, CertPro’s understanding of the HKMA’s third-party risk management framework and the SFC’s operational resilience guidelines enables the audit team to structure the engagement scope and report content in a manner that directly addresses regulators’ evidence requirements.

This regulatory alignment ensures that the resulting attestation report provides maximum utility to the service organization’s financial sector clients during vendor assessments and annual reviews.

Steps to Obtain SOC 2 Certification in Hong Kong

Organizations pursuing SOC 2 Certification in Hong Kong follow a defined sequence of activities from initial scoping through report issuance. Each step in this process serves a specific purpose in the overall attestation engagement and contributes to the accuracy and reliability of the final report. The following steps describe the engagement process as it applies to organizations working with CertPro as the engaged Licensed CPA Firm.

- Determine the Trust Services Criteria applicable to the organization’s services and customer commitments

- Define the system boundary, identifying all infrastructure, applications, personnel, and procedures within scope

- Confirm the audit type — SOC 2 Type I for point-in-time assessment or SOC 2 Type II for operating effectiveness over a defined period

- Establish the audit observation period start date and ensure controls are consistently operated from that date

- Collect and organize all required policy documentation, procedure records, and technical configuration evidence

- Engage CertPro as the Licensed CPA Firm to conduct the formal SOC 2 audit engagement

- Participate in the audit walkthrough process, providing documentation and personnel access as required by the auditor

- Review the draft system description prepared by management for accuracy and completeness

- Respond to auditor inquiries during operating effectiveness testing, providing evidence artifacts for each sampled control instance

- Review the draft attestation report and provide management’s response to any exceptions identified

- Receive the final SOC 2 attestation report and distribute to authorized parties under applicable confidentiality agreements

- Initiate planning for the subsequent annual audit cycle to maintain continuous attestation coverage

FAQ

▶

What is SOC 2 Certification and who needs it in Hong Kong?

▶

How long does a SOC 2 audit take in Hong Kong?

▶

What is the difference between SOC 2 Type I and Type II in Hong Kong?

▶

Is SOC 2 a legal requirement for businesses in Hong Kong?

▶

Can a Hong Kong-based organization obtain SOC 2 certification?

▶

How does SOC 2 relate to Hong Kong’s Personal Data (Privacy) Ordinance?

▶

What happens if exceptions are found during a SOC 2 audit?

▶

How frequently must SOC 2 audits be conducted to maintain current status?

SOC 1 VS SOC 2: WHICH REPORT YOUR CUSTOMERS ACTUALLY ASK FOR

If you sell SaaS or provide outsourced services, you have likely been asked for a SOC report. However, the follow-up question is rarely easy to answer…

Secure Email Platform Exclaimer Renews ISO, SOC 2

Excerpt from The Manila Times Article, Published on February 26, 2026 Secure email solutions provider Exclaimer has renewed its ISO and SOC 2 certific…

SOC 2 FRAMEWORK REQUIREMENTS IN 2026. WHAT HAS CHANGED?

Security reviews used to happen at the tail end of a deal. Today, they happen in the first conversation. Enterprise buyers come prepared. They ask abo…

Get In Touch

have a question? let us get back to you.