A SOC 2 report is now a standard requirement in enterprise technology procurement. SOC 2 report quality, however, is not standard — and the difference is consequential. Buyers request it before contracts proceed. Vendor risk teams review it alongside security questionnaires. Legal diligence teams examine it during M&A reviews. The report has become a trust document — a professional attestation that sits at the center of vendor selection and renewal decisions across industries.

In 2026, that trust is under scrutiny. The AICPA Peer Review Board has issued direct guidance to peer reviewers on how to evaluate risks in SOC 2 engagements, particularly those involving third-party compliance platforms and bundled service arrangements. The Journal of Accountancy has published three articles in 2026 alone addressing threats to SOC 2 report quality — covering fast-and-easy market promises, ethics risks in tool provider arrangements, and the AICPA's enhanced oversight approach.

The underlying issue is structural. As SOC 2 demand has grown, a market has developed around making the process faster, cheaper, and more standardized. Platform vendors, bundled packages, and fixed timelines have entered the space with marketing claims that compress a complex examination into weeks. Some of that efficiency is legitimate. Some of it is not — and the AICPA's recent attention makes clear that the profession is drawing the line on what constitutes acceptable SOC 2 report quality.

For buyers, this matters more than many procurement teams realize. A SOC 2 report that satisfies an intake checklist is not the same as a report that withstands detailed vendor risk review, legal diligence scrutiny, or enterprise security team examination. Understanding what SOC 2 report quality actually requires — and how to evaluate it — is now a practical procurement competency, not a compliance formality.

Concern

SOC 2 report quality is at risk in a market where compliance tool vendors, bundled packages, and fixed timelines have created pressure on auditors to compress examination scope, reduce evidence testing, and issue standardized reports. The AICPA Peer Review Board has responded with enhanced oversight of SOC 2 engagements and direct guidance to peer reviewers on evaluating quality risks — including tool-driven timelines, referral arrangements, and boilerplate report content.

Overview

SOC 2 report quality depends on three foundational elements: auditor independence from the service organization and any tool provider, rigorous evidence testing against the actual control environment, and a system description and scope tailored to the specific organization's systems and risks. Reports that lack any of these elements may satisfy a procurement checkbox but fail under close review by enterprise legal, security, or vendor risk teams.

Solution

Buyers should evaluate SOC 2 reports and the engagement structures that produced them, not just the final document. Key indicators of a quality report include a tailored system description, a clear and defined audit period, documented test procedures for each control, and a service auditor who is a licensed CPA firm enrolled in the AICPA Peer Review Program — with no financial dependency on or referral relationship with any compliance tool provider.

What Is a SOC 2 Type 2 Report and What It Must Contain

What is a SOC 2 Type 2 report? It is an independent attestation issued by a licensed CPA firm under AICPA Statements on Standards for Attestation Engagements, specifically AT-C Section 205.

The report evaluates whether a service organization's controls were not just designed appropriately but operated effectively throughout a defined examination period. This is what distinguishes a Type 2 report from a Type 1: Type 1 captures control design at a single point in time; Type 2 tests operating effectiveness over a sustained period.

The SOC 2 audit process produces a report that contains four primary components.

- The auditor's opinion is the professional conclusion on whether controls operated effectively.

- The management assertion is the service organization's own representation about its control environment.

- The system description defines what was in scope — which systems, personnel, processes, and infrastructure the examination covered.

- The description of tests performed and results details how the auditor evaluated each control and what the testing found.

SOC 2 report quality depends significantly on how rigorously each of these components is produced and how accurately they reflect the organization being examined.

Understanding what is a SOC 2 Type 2 report also means understanding what it does not provide. A SOC 2 report is not a certification. It does not guarantee that no security incidents will occur. It does not cover systems outside its defined scope. It reflects the auditor's professional judgment about control effectiveness during the examination period — a judgment that is only as reliable as the independence, rigor, and professional competence of the firm that issued it.

What SOC 2 Report Quality Actually Means

SOC 2 report quality is not determined by how quickly an examination is completed, the sophistication of the technology used, or the appearance of the final report. Instead, it depends on whether the auditor independently evaluated the controls operating within the organization's environment, obtained sufficient evidence to support the conclusions reached, and applied professional judgment throughout the engagement.

This distinction sits at the center of recent discussions about the SOC 2 audit process. The concern is not the use of automation. Evidence collection platforms can improve efficiency, centralize documentation, and reduce administrative effort. The concern arises when technology begins to influence audit conclusions or restrict an auditor's ability to expand testing, investigate exceptions, or tailor procedures to the organization's unique environment.

Recent guidance from the AICPA Peer Review Board reinforces this point. SOC 2 report quality depends on whether examination timelines are reasonable, whether the system description accurately reflects the organization's environment, and whether testing is designed around actual control activities rather than predefined workflows. These same indicators can help buyers understand how to evaluate a SOC 2 report before relying on it.

What Low-Quality Reports Look Like in Practice

Many SOC 2 report quality issues are visible within the report itself. Generic system descriptions that provide little detail about the product, infrastructure, or subservice organizations often suggest a template-driven approach. Test procedures that rely heavily on inquiry with limited independent verification may indicate shallow testing.

Similarly, report language that appears nearly identical across multiple vendors can raise questions about the level of auditor judgment applied during the examination. When security, procurement, and legal teams encounter these warning signs, they often request additional evidence or determine that the report is insufficient for vendor approval.

SOC 2 Auditor Independence: The Foundation of Report Credibility

SOC 2 auditor independence is not an administrative requirement. It is the foundation of trust behind every SOC 2 report. A licensed CPA firm performing an attestation engagement must remain independent of both the organization being examined and any third party that could influence the auditor's judgment. This independence is what separates a SOC 2 report from a self-assessment, readiness review, or compliance dashboard. Ultimately, SOC 2 report quality depends on whether that independence exists in practice, not simply on paper.

Recent industry discussions have highlighted several threats to SOC 2 auditor independence that can emerge in tool-provider relationships. An undue influence threat arises when a platform provider can affect decisions related to scope, testing, timing, evidence, or conclusions. A self-interest threat may develop when referral arrangements, compensation structures, or revenue dependencies create financial incentives that could influence professional judgment. A familiarity threat can occur when auditors become overly reliant on predefined workflows rather than evaluating each organization's unique control environment.

These risks matter because independence is central to the credibility of the SOC 2 audit process. Professional judgment must be driven by the evidence obtained during the examination, not by the technology supporting it.

For buyers, the implications are straightforward. Only licensed CPA firms can issue SOC 2 attestation reports under AICPA standards. Compliance platforms, readiness tools, and advisory firms cannot issue a SOC 2 report regardless of how their services are marketed. When considering how to evaluate a SOC 2 report, buyers should confirm that the issuing firm is a licensed CPA firm, maintains active peer review standing, and operates free from financial relationships that could compromise auditor independence.

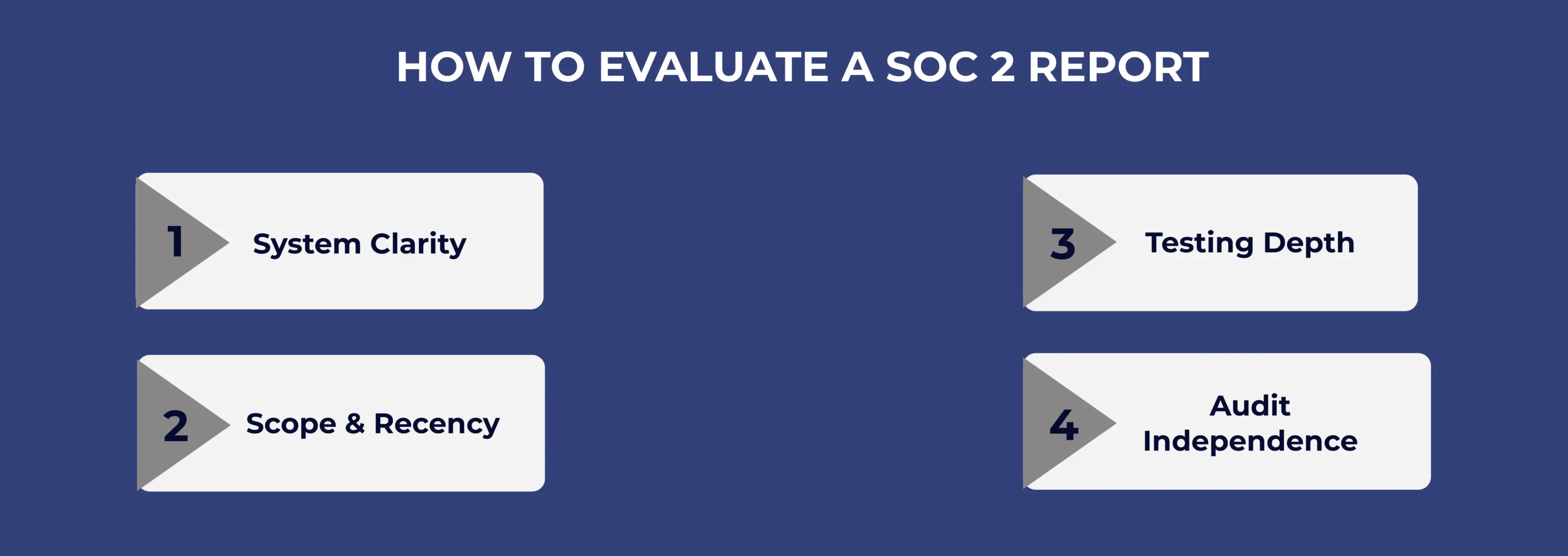

How to Evaluate a SOC 2 Report

Knowing how to evaluate a SOC 2 report is now an essential skill for vendor risk managers, procurement teams, and enterprise security professionals. SOC 2 report quality cannot be judged simply by the existence of a report. It must be evaluated through the contents of the report and the structure of the engagement behind it.

-

System Clarity

A high-quality system description should clearly identify the product or service being examined, the infrastructure supporting it, the teams responsible for operating controls, and any subservice organizations involved. A strong SOC 2 report example should also identify the cloud environment, the data types in scope, and any exclusions or carve-outs. Generic descriptions that could apply to almost any SaaS provider deserve closer scrutiny because they may reveal a template-driven approach.

-

Scope and Recency

Review whether the Trust Services Criteria align with the vendor's business activities and the data they handle. The examination period also matters. What is a SOC 2 type 2 report if not an assessment of controls operating over time? A report that is more than twelve months old may provide limited assurance about the current state of the control environment. Scope, coverage, and timeliness are all important indicators of SOC 2 report quality.

-

Testing Depth

The tests of controls section often provides the clearest view of SOC 2 report quality. A strong SOC 2 report example should describe the testing procedures performed, the evidence sampled, the sample size selected, and any exceptions identified. Reports that rely heavily on management inquiry without independent evidence verification may indicate limited examination depth. Testing should also reflect risk. Higher-risk controls should receive greater scrutiny than lower-risk controls.

-

Audit Independence

How to evaluate a SOC 2 report extends beyond the document itself. Confirm that the issuing organization is a licensed CPA firm and participates in the AICPA Peer Review Program. Buyers should also understand whether any referral arrangements or financial relationships exist between the auditor and the compliance platform used by the vendor. SOC 2 auditor independence is a foundational component of SOC 2 report quality. If independence cannot be verified, the credibility of the report deserves additional examination.

SOC 2 Report Quality vs Speed: Where the Market Has Shifted

The debate around SOC 2 audit quality vs speed has become one of the defining issues in today's compliance market. As demand for SOC 2 reports continues to grow, many organizations face pressure to complete examinations quickly in order to satisfy customer and procurement requirements.

The challenge arises when speed becomes the primary objective of the engagement. Fixed timelines established before an auditor fully understands the system can limit the scope of testing. Predefined workflows may reduce flexibility when unusual control designs or exceptions emerge. Compressed schedules can also leave less time to investigate inconsistencies, perform follow-up testing, or evaluate evidence that does not align with expectations.

For service organizations, the tradeoff is real. Enterprise customers often require a SOC 2 report before moving forward with contracts, making the fastest path highly attractive. However, a report that satisfies an intake checklist may not withstand deeper scrutiny from a sophisticated security team, legal department, or vendor risk program.

When concerns about SOC 2 report quality emerge during customer reviews, the consequences can be significant. Procurement timelines may extend, additional evidence may be requested, and contract approvals can be delayed. In some cases, organizations face costly remediation efforts while under business pressure to close a deal.

The key distinction is that efficiency and quality are not the same thing. A streamlined SOC 2 audit process can support strong outcomes when auditors maintain appropriate scope, test sufficient evidence, evaluate exceptions, and exercise independent judgment. Problems arise when speed is achieved by reducing audit rigor. From a SOC 2 audit quality vs speed perspective, that is where report credibility begins to erode.

Conclusion

SOC 2 report quality is ultimately a measure of trust. Buyers do not rely on a report because it exists. They rely on it because they believe the examination was conducted independently, supported by sufficient evidence, and guided by professional judgment.

Recent actions by the AICPA Peer Review Board reinforce an important message for the market: audit quality cannot be sacrificed for speed, convenience, or standardized workflows. Technology can improve efficiency within the SOC 2 audit process, but it cannot replace the independence, skepticism, and judgment that give an attestation report its credibility.

For service organizations, the implications are practical. A report that fails enterprise security review, triggers additional vendor risk assessments, or raises concerns during legal diligence often creates far greater costs than investing in a rigorous examination from the outset. When evaluating SOC 2 audit quality vs speed, organizations should focus on whether the report can withstand scrutiny from customers, procurement teams, and security stakeholders long after it is issued.

At CertPro CPA LLC, we issue SOC 2 attestation reports directly as a licensed CPA firm under AICPA attestation standards. We are enrolled in the AICPA Peer Review Program and conduct evidence-based examinations tailored to each organization's specific control environment. Our approach is built on auditor independence, documented evidence, and professional accountability because these principles remain the foundation of every credible SOC 2 report.

In the end, SOC 2 report quality is not determined by how quickly a report is delivered. It is determined by whether the report continues to hold value when the scrutiny begins.