SOC 2 Certification in Wilmington

CertPro is a Licensed CPA Firm conducting SOC 2 certification audits for service organizations operating in Wilmington. Evaluations are structured against the AICPA Trust Services Criteria, covering security, availability, confidentiality, processing integrity, and privacy. SOC 2 attestation reports are issued following independent audit procedures applicable to Wilmington-based technology, financial services, and data-driven organizations seeking credible, third-party verified compliance documentation.

OUR CLIENTS

Introduction to SOC 2 Certification in Wilmington

SOC 2 Certification in Wilmington represents a formal attestation issued by a licensed CPA firm confirming that a service organization’s information systems meet the AICPA Trust Services Criteria (TSC). The certification applies to organizations that store, process, or transmit customer data through technology-based service delivery models. In Wilmington, Delaware — a recognized hub for financial services, banking institutions, and technology-driven enterprises — SOC 2 attestation has become a baseline requirement for organizations seeking to establish credibility with enterprise clients and regulated entities.

Wilmington’s unique business landscape includes major credit card companies, national banks, insurance firms, and a rapidly expanding fintech sector. This environment creates significant demand for independent, third-party data security verification. SOC 2 compliance in this context is not merely a market differentiator — it is increasingly a contractual prerequisite imposed by enterprise procurement teams, financial regulators, and institutional clients. Organizations pursuing SOC 2 Certification in Wilmington must demonstrate that their controls around security, availability, confidentiality, processing integrity, and privacy operate effectively over a defined audit period.

What Is SOC 2?

SOC 2 — System and Organization Controls 2 — is an auditing standard developed by the American Institute of Certified Public Accountants (AICPA). It defines criteria for managing customer data based on five Trust Services Criteria: Security, Availability, Processing Integrity, Confidentiality, and Privacy. Unlike prescriptive compliance frameworks, SOC 2 is principles-based. Each organization defines its own controls, and the auditor evaluates whether those controls are suitably designed and operating effectively against the defined criteria.

A SOC 2 audit produces an attestation report — not a certification in the traditional sense — prepared exclusively by a licensed CPA firm. The report provides a formal opinion on whether a service organization’s controls meet the Trust Services Criteria over a specified review period. For Wilmington companies operating in banking, fintech, healthcare technology, and SaaS sectors, a SOC 2 report functions as authoritative evidence that data protection commitments are substantiated through independent evaluation, not self-certification.

SOC 2 Type I vs. SOC 2 Type II: Key Distinctions

SOC 2 audit engagements are conducted under two distinct report types. A SOC 2 Type I audit evaluates whether an organization’s controls are suitably designed as of a specific point in time. It confirms that the control environment exists and is structured appropriately, but does not assess whether controls operated effectively over an extended period. A SOC 2 Type I audit in Wilmington is typically the starting point for organizations new to the SOC 2 process and seeking to demonstrate baseline control design to prospective clients.

A SOC 2 Type II engagement in Wilmington covers a defined observation period — typically six to twelve months — during which the auditor evaluates both the design and the operating effectiveness of controls. Type II reports carry significantly greater assurance value because they demonstrate sustained control performance rather than a single-point-in-time snapshot. Wilmington-based financial services companies and technology providers are most frequently required to furnish Type II reports to enterprise clients and regulated counterparties. Most institutional procurement requirements in Delaware’s financial sector specifically mandate Type II attestation.

| Attribute | SOC 2 Type I | SOC 2 Type II |

|---|---|---|

| Evaluation Scope | Control design at a point in time | Design and operating effectiveness over a period |

| Observation Period | Single date | Typically 6–12 months |

| Assurance Level | Moderate | High |

| Common Use Case | Initial market entry or new client requirements | Enterprise contracts and regulated client relationships |

| Report Frequency | One-time or transitional | Annual renewal typical |

SOC 2 and Wilmington’s Regulatory Environment

Wilmington, Delaware operates within a dense regulatory environment shaped by federal financial regulations, state-level data protection requirements, and industry-specific security mandates. Organizations subject to Gramm-Leach-Bliley Act (GLBA) obligations, PCI DSS requirements, or HIPAA controls frequently pursue SOC 2 compliance in Wilmington as a complementary attestation that addresses information security controls across their full service delivery footprint. SOC 2 attestation provides a structured, independently verified record of control performance that satisfies both regulatory auditors and client security review teams.

Delaware serves as the legal domicile for more than 60% of Fortune 500 companies and nearly all major U.S. financial institutions. This creates a unique ecosystem in which data security attestation is embedded in vendor onboarding, third-party risk management, and supply chain due diligence processes. Wilmington-based service organizations without a current SOC 2 attestation report frequently encounter procurement barriers that limit their ability to serve financial institutions, healthcare networks, and government contractors in the region. SOC 2 Certification in Wilmington is therefore both a risk management instrument and a commercial enabler.

Benefits of SOC 2 Certification in Wilmington

The benefits of SOC 2 Certification in Wilmington extend across commercial, operational, and risk management dimensions. For organizations operating in Delaware’s highly concentrated financial services market, an independently issued SOC 2 attestation report communicates a level of control assurance that self-assessment or internal audits simply cannot replicate. The report provides documented evidence that a licensed CPA firm has evaluated the organization’s information security infrastructure and issued a formal opinion based on the AICPA Trust Services Criteria.

SOC 2 certification for Wilmington companies unlocks access to enterprise client segments that require independent security attestation as a condition of vendor approval. Financial institutions headquartered in Wilmington — including credit card issuers, commercial banks, and insurance holding companies — routinely include SOC 2 Type II report requirements in their third-party vendor agreements. Technology providers, managed service organizations, and SaaS platforms that can produce a current SOC 2 report reduce procurement cycle times and avoid remediation requests that delay contract execution.

For Wilmington fintech companies competing for contracts with nationally chartered banks and investment firms, achieving SOC 2 compliance provides a measurable competitive advantage. Organizations that hold a current Type II attestation can present independently verified evidence of their security posture during RFP processes, security questionnaire reviews, and enterprise due diligence evaluations. This reduces reliance on self-reported security metrics and replaces lengthy vendor security questionnaires with a single authoritative document issued by a licensed CPA firm.

The SOC 2 audit process requires organizations to formally document their control environment, assign control ownership, establish evidence collection procedures, and demonstrate continuous control operation. This discipline produces measurable improvements in operational risk management, incident response preparedness, and internal audit readiness. Organizations that complete a SOC 2 audit in Wilmington typically emerge with a more structured understanding of their control gaps, a clearer accountability framework, and documented evidence that supports both internal governance and external reporting requirements.

SOC 2 compliance also supports alignment with other regulatory frameworks applicable to Wilmington businesses. Organizations subject to Delaware’s data breach notification laws, federal financial privacy regulations, or sector-specific cybersecurity requirements — such as the NYDFS Cybersecurity Regulation affecting entities with New York nexus — benefit from the control documentation and testing evidence generated through the SOC 2 audit process. The structured evidence record produced during a SOC 2 engagement is directly applicable to regulatory examinations, internal audit cycles, and board-level risk reporting.

SOC 2 attestation directly addresses the trust deficit that exists in B2B technology and service relationships where one organization’s security posture materially affects another’s data protection obligations. For Wilmington-based organizations that process financial data, health information, or personally identifiable information on behalf of clients, a SOC 2 report provides clients with independently verified assurance that contractual security commitments are substantiated by tested controls — not merely stated in service agreements.

- ✓Independently verified evidence of security control effectiveness for client due diligence

- ✓Reduced vendor security questionnaire burden through standardized attestation reporting

- ✓Accelerated enterprise sales cycles by satisfying procurement security requirements upfront

- ✓Demonstrated alignment with AICPA Trust Services Criteria for all five control categories

- ✓Support for regulatory examination readiness across federal and state compliance obligations

- ✓Formal basis for cyber insurance underwriting and premium positioning

- ✓Board-level assurance documentation for governance, risk, and compliance reporting

- ✓Competitive differentiation in Wilmington’s financial services and fintech vendor marketplace

- ✓Annual audit cycle discipline that strengthens internal control environments over time

- ✓Third-party risk management credibility for clients managing vendor security programs

- ✓Commercial and Market Access Benefits

- ✓Risk Management and Internal Control Benefits

- ✓Client Trust and Contractual Assurance Benefits

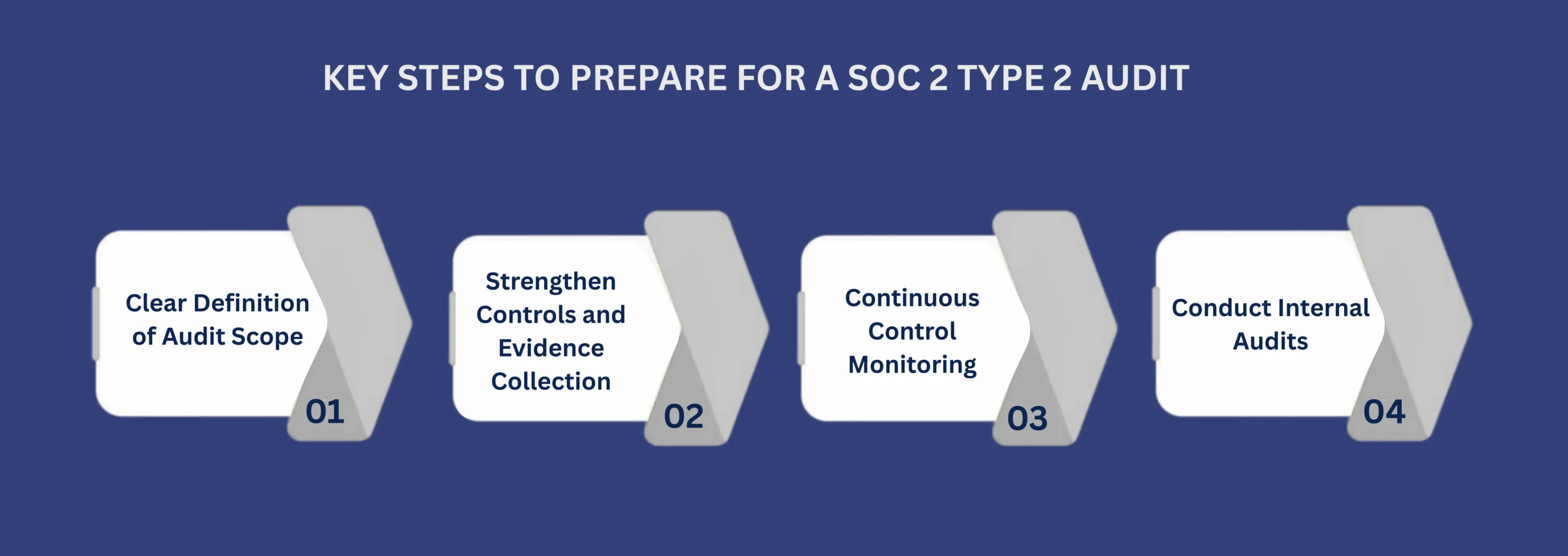

SOC 2 Audit Process for Wilmington Organizations

The SOC 2 audit process for Wilmington-based organizations follows a structured sequence of evaluation stages defined by the AICPA’s attestation standards and the applicable Trust Services Criteria. Each stage is conducted by a licensed CPA firm and produces documented findings that inform the final attestation report. Understanding the full audit sequence enables organizations to allocate resources appropriately, establish internal accountability for control evidence, and manage audit timelines effectively across their business operations.

The SOC 2 audit engagement begins with a formal scope definition process in which the auditor and the organization jointly establish the boundaries of the system under review. Scope definition identifies the specific services, infrastructure components, data flows, and organizational units that fall within the audit boundary. For Wilmington organizations operating across multiple service lines or technology environments, precise scope definition is essential to ensure the resulting attestation report accurately reflects the evaluated control environment and meets the expectations of intended report users.

Concurrent with scope definition, the organization and auditor determine which Trust Services Criteria categories apply to the engagement. The Security criterion (Common Criteria) is mandatory for all SOC 2 audits. Additional criteria — Availability, Processing Integrity, Confidentiality, and Privacy — are included based on the nature of services delivered, the commitments made to clients, and applicable regulatory requirements. Wilmington financial services companies frequently include Confidentiality and Availability criteria given their obligations to safeguard financial data and maintain system uptime commitments.

Following scope confirmation, the licensed CPA firm develops an audit program specifying the control domains to be evaluated, the testing procedures to be applied, and the evidence types required to satisfy each criterion. The audit program is structured around the AICPA’s Trust Services Criteria point-of-focus requirements, which define the attributes auditors must assess for each applicable criterion. Evidence planning identifies the specific documentation, system logs, configuration records, and personnel interviews required to substantiate control design and operating effectiveness.

For SOC 2 audit engagements in Wilmington, Delaware, the audit program accounts for the specific technology infrastructure, third-party service provider relationships, and operational characteristics of the organization under review. Organizations that rely on cloud infrastructure providers, co-location data centers, or subservice organizations must address how those third-party relationships are managed within their control environment. The auditor’s program will include procedures for evaluating vendor management and subservice organization monitoring controls accordingly.

Control testing is the core evaluative phase of the SOC 2 audit. For Type II engagements, the auditor evaluates evidence collected across the full observation period to determine whether controls operated effectively on a consistent basis. Testing procedures include inspection of documentation and system-generated records, re-performance of control procedures using population samples, observation of operational processes, and inquiry of personnel responsible for control execution. Each tested control must produce sufficient, appropriate evidence to support the auditor’s findings.

Evidence evaluation during the SOC 2 audit involves assessing whether evidence collected demonstrates that controls addressed the specific risks identified in the audit program. The auditor evaluates the completeness of the evidence population, the consistency of control operation across the observation period, and the absence of material deviations or control failures. Where deviations are identified, the auditor documents the nature of the deviation, its potential impact on the applicable Trust Services Criterion, and whether it constitutes a control deficiency material to the audit opinion.

Following control testing, the auditor communicates identified control deficiencies or exceptions to the organization’s management for review and response. Management reviews each finding, confirms factual accuracy, and provides written responses that acknowledge the finding, describe any corrective actions taken during the observation period, and outline remediation plans for deficiencies not yet addressed. This iterative review process ensures the final attestation report accurately reflects the control environment and that management’s perspective is documented within the report.

The final stage of the SOC 2 audit process produces the formal attestation report, which includes the licensed CPA firm’s opinion on whether the service organization’s controls meet the applicable Trust Services Criteria. The report comprises several sections: the independent service auditor’s report (containing the audit opinion), management’s assertion regarding the system description and control effectiveness, the system description prepared by management, and the description of tests of controls and results prepared by the auditor. The SOC 2 attestation report for Wilmington organizations is issued under AICPA AT-C Section 205 attestation standards.

The audit opinion may be unqualified (a clean opinion confirming controls meet criteria), qualified (confirming controls meet criteria except for identified exceptions), adverse (indicating controls do not meet criteria), or disclaimed (indicating insufficient evidence to form an opinion). For organizations seeking to use their SOC 2 report in client procurement processes or regulatory submissions, an unqualified opinion is the expected outcome. Organizations with qualified opinions must address the underlying control deficiencies to achieve a fully clean attestation in subsequent audit cycles.

- ✓Stage 1: Scope Definition and Trust Services Criteria Selection

- ✓Stage 2: Audit Program Determination and Evidence Planning

- ✓Stage 3: Control Testing and Evidence Evaluation

- ✓Stage 4: Nonconformity Review and Management Response

- ✓Stage 5: Attestation Report Issuance and Certification Decision

SOC 2 Requirements for Wilmington Service Organizations

SOC 2 compliance requirements are defined by the AICPA Trust Services Criteria and applied to the specific control environment of each organization undergoing audit. Unlike prescriptive compliance frameworks, SOC 2 does not specify particular security technologies or configurations. Instead, it requires organizations to implement controls that are suitably designed and operating effectively to meet their service commitments and system requirements. For SOC 2 Certification in Wilmington, organizations must satisfy requirements across control documentation, technical safeguards, operational procedures, and personnel accountability.

SOC 2 documentation requirements establish that organizations maintain formal written records of their policies, procedures, and control activities. Required documentation includes an information security policy that addresses the full scope of the Trust Services Criteria, asset management procedures, access control policies, change management procedures, incident response plans, vendor management policies, and business continuity and disaster recovery plans. Each document must be formally approved, version-controlled, and demonstrably communicated to relevant personnel.

For SOC 2 audit engagements in Wilmington, documentation must also include the system description — a management-prepared narrative describing the services provided, the infrastructure components involved, the relevant aspects of the control environment, and the complementary user entity controls (CUECs) that clients must implement to achieve the stated control objectives. The system description forms a foundational element of the SOC 2 report and must accurately represent the organization’s actual operational environment as of the audit date or throughout the observation period.

Technical requirements for SOC 2 compliance encompass the specific security controls implemented within an organization’s technology infrastructure. Under the Security criterion’s Common Criteria, organizations must demonstrate controls across nine control categories: organization and management, communications, risk management, monitoring of controls, logical and physical access controls, system operations, change management, risk mitigation, and additional criteria specific to the applicable TSC categories. Each category requires documented evidence that controls exist and operate in the manner described.

For Wilmington technology companies operating cloud-based infrastructure, technical requirements include demonstrated controls over identity and access management, encryption of data in transit and at rest, network segmentation and perimeter security, vulnerability management and patch cycle documentation, security monitoring and logging with defined retention periods, and multi-factor authentication enforcement for privileged access. Organizations that process financial data or host sensitive client information in Wilmington data centers must also address physical access controls, environmental monitoring, and data center redundancy as part of their Availability criterion controls.

SOC 2 operational requirements address how an organization’s personnel execute and monitor controls on a day-to-day basis. Requirements include background screening procedures for personnel with access to sensitive systems, security awareness training programs with documented completion records, defined roles and responsibilities for control ownership, segregation of duties for critical financial and system administration functions, and formal performance evaluation processes that include security accountability. Personnel-related controls are evaluated through documentation review, inquiry, and evidence of consistent execution across the observation period.

- ✓Formally documented information security policy covering all applicable Trust Services Criteria

- ✓Written access control procedures with defined provisioning, review, and deprovisioning workflows

- ✓Incident response plan with documented test records and post-incident review procedures

- ✓Change management procedures with documented approval workflows and rollback provisions

- ✓Vendor and subservice organization management policy with periodic assessment documentation

- ✓Business continuity and disaster recovery plans with tested recovery time objectives

- ✓Security awareness training program with completion tracking and periodic update cycles

- ✓Risk assessment process with documented methodology, frequency, and output records

- ✓Vulnerability management program with defined scan frequency and remediation timelines

- ✓Audit log management with defined retention periods and integrity protection controls

- ✓Documentation Requirements

- ✓Technical and Infrastructure Requirements

- ✓Operational and Personnel Requirements

SOC 2 Certification Cost in Wilmington

The cost of SOC 2 Certification in Wilmington varies based on several organizational and audit-scope factors — including the size and complexity of the system under review, the number of Trust Services Criteria included in the engagement, whether the organization pursues a Type I or Type II report, and the maturity of the existing control environment. Organizations with well-documented control frameworks, established audit evidence processes, and limited subservice organization dependencies typically incur lower audit costs than those with complex environments requiring extensive testing procedures.

Factors That Influence SOC 2 Audit Costs

The primary cost drivers for a SOC 2 audit engagement include the scope of the system description, the number and complexity of controls subject to testing, the duration of the observation period for Type II engagements, and the volume of evidence sampling required. Organizations with larger personnel populations, more complex technology architectures, or greater numbers of subservice organizations require more extensive testing procedures and correspondingly higher audit investment. Wilmington financial services companies with large transaction processing environments or multi-cloud infrastructure footprints typically fall into higher-complexity audit categories.

Additional cost considerations include the organization’s internal resource availability for audit coordination, the completeness of existing documentation, and whether prior SOC 2 reports exist that can inform the current engagement. Organizations undergoing their first SOC 2 audit typically invest more time in system description development, evidence collection process establishment, and control documentation formalization. Subsequent annual audit cycles — required to maintain current SOC 2 Type II certification status — tend to be more efficient as evidence collection processes are established and control documentation is maintained on an ongoing basis.

| Organization Profile | Report Type | Typical Audit Cost Range | Key Cost Drivers |

|---|---|---|---|

| Small SaaS or fintech startup | Type I | $15,000–$30,000 | First-time engagement, limited control documentation |

| Mid-size technology provider | Type II | $30,000–$60,000 | Extended observation period, multiple TSC categories |

| Large financial services firm | Type II | $60,000–$120,000+ | Complex infrastructure, multiple subservice organizations |

| Enterprise data processor | Type II (annual) | $50,000–$90,000 | High evidence volume, regulatory-grade testing procedures |

SOC 2 Certification Cost vs. Value for Wilmington Businesses

For Wilmington organizations evaluating the return on investment of a SOC 2 audit engagement, the relevant comparison is not solely the direct audit cost but also the commercial value enabled by holding a current attestation report. Organizations that secure enterprise contracts requiring SOC 2 Type II reports, avoid data breach incidents through the control discipline enforced by the audit process, or reduce cyber insurance premiums through documented control effectiveness frequently find that the audit investment is fully justified by these downstream commercial and risk management outcomes.

CertPro, operating as a Licensed CPA Firm, structures SOC 2 audit engagements to align with the specific complexity profile and budget parameters of each Wilmington client organization. Engagement scope, audit procedures, and evidence collection requirements are defined in advance to provide cost predictability throughout the audit cycle. Organizations in Wilmington’s banking sector, technology industry, and healthcare technology space benefit from CertPro’s established audit methodology, which is calibrated to the Trust Services Criteria and applicable attestation standards without unnecessary scope expansion.

SOC 2 Compliance in Wilmington’s Financial Services Sector

SOC 2 compliance engagements for Wilmington financial services organizations reflect the specific data security and operational control requirements that apply within Delaware’s concentrated financial sector. Wilmington serves as the legal and operational headquarters for some of the largest credit card issuers, commercial banks, and consumer financial companies in the United States. Service organizations — including technology vendors, payment processors, data analytics firms, and managed service providers — that serve these institutions must maintain SOC 2 attestation as a condition of ongoing vendor relationships.

SOC 2 Requirements for Wilmington Banking Sector Vendors

SOC 2 certification requirements for Wilmington’s banking sector are driven by the third-party risk management programs maintained by regulated financial institutions. Banks and credit card companies operating in Wilmington implement formal vendor due diligence processes that require service providers to demonstrate independent security attestation before being approved as authorized vendors. SOC 2 Type II reports are the standard attestation document requested, with annual renewal required to maintain approved vendor status. Organizations that allow their SOC 2 report to lapse face re-qualification requirements that delay service delivery and create commercial risk.

The Office of the Comptroller of the Currency (OCC) and the Federal Reserve’s supervisory guidance on third-party risk management have established clear expectations for how nationally chartered banks — many of which are headquartered or operating in Wilmington — manage vendor security risk. These guidelines explicitly reference independent attestation reports, including SOC 2, as appropriate mechanisms for vendor security evaluation. Wilmington-based technology vendors and service providers that hold current SOC 2 attestation reports are better positioned to satisfy their banking clients’ regulatory compliance obligations.

SOC 2 Compliance for Wilmington Fintech Companies

SOC 2 compliance for Wilmington fintech organizations presents a dual mandate: demonstrating security assurance to enterprise banking clients while also meeting the expectations of investors, board members, and regulatory examiners who evaluate risk management maturity. Fintech companies in Wilmington that process payment transactions, manage digital wallets, operate lending platforms, or provide financial data aggregation services handle sensitive financial data subject to multiple regulatory regimes. SOC 2 attestation provides a structured control evaluation framework that addresses security and data handling requirements across these overlapping obligations.

For early-stage fintech organizations in Wilmington, initiating the SOC 2 process with a Type I audit provides an initial attestation that can be presented to prospective banking partners and institutional investors while the organization builds toward a Type II observation period. The Type I audit establishes the system description, identifies applicable Trust Services Criteria, and confirms that controls are suitably designed. This creates a documented foundation that accelerates the subsequent Type II audit cycle and demonstrates proactive security governance to key stakeholders.

SOC 2 and Delaware Data Center Operators

Data center operators and co-location service providers in the Wilmington and greater Delaware region frequently pursue SOC 2 attestation to address the security assurance requirements of their financial services, healthcare, and government clients. For data center organizations, the Availability and Confidentiality criteria are particularly relevant alongside the mandatory Security criterion. Clients require assurance that hosted systems remain accessible, environmental controls protect physical assets, and logical access controls prevent unauthorized access to co-located client systems.

SOC 2 vs. ISO 27001: Choosing the Right Framework for Wilmington Organizations

Organizations pursuing information security attestation frequently evaluate SOC 2 and ISO 27001 as alternative or complementary frameworks. For Wilmington-based organizations serving the U.S. financial services market, SOC 2 is the dominant standard requested by enterprise clients and regulated institutions. ISO 27001 provides a globally recognized certification valued by international clients and multinational enterprises, but does not carry the same specific assurance weight in U.S. financial services vendor due diligence processes that SOC 2 attestation does.

Framework Comparison: SOC 2 vs. ISO 27001

SOC 2 is issued by a licensed CPA firm under AICPA attestation standards and produces a detailed report describing the system, the controls tested, and the auditor’s opinion on control effectiveness. ISO 27001 is a certification issued by an accredited certification body following an audit against the ISO 27001 Information Security Management System standard. SOC 2 reports are shared directly with intended users — typically enterprise clients — under non-disclosure provisions, while ISO 27001 certificates are publicly verifiable through the certification body’s registry.

| Dimension | SOC 2 | ISO 27001 |

|---|---|---|

| Issuing Body | Licensed CPA Firm (AICPA standards) | Accredited Certification Body (ISO/IEC) |

| Geographic Relevance | Dominant in U.S. financial services market | Global recognition, especially in Europe and Asia |

| Report Format | Detailed attestation report shared with clients | Public certificate with surveillance audits |

| Control Specificity | Tests specific controls based on TSC and service commitments | Evaluates ISMS implementation against ISO 27001 Annex A |

| Renewal Cycle | Annual for Type II reports | Three-year certification cycle with annual surveillance |

Wilmington organizations with international operations, European client relationships, or plans to expand into global markets frequently pursue both SOC 2 and ISO 27001. The two frameworks are complementary: the control documentation and evidence collection processes developed for one framework significantly reduce the incremental effort required for the other. Organizations that have already built control libraries, policy frameworks, and audit evidence processes for SOC 2 compliance are well-positioned to pursue ISO 27001 certification using the same control infrastructure, with modifications to address ISO-specific requirements.

When SOC 2 Takes Priority Over ISO 27001

SOC 2 takes priority when the organization’s primary client base consists of U.S. financial institutions, healthcare organizations, or technology companies that specifically require SOC 2 attestation in vendor agreements. In Wilmington’s financial services environment, SOC 2 is the standard security attestation document embedded in third-party risk management programs. Organizations that pursue ISO 27001 first without addressing their clients’ specific SOC 2 requirements may find that ISO certification does not satisfy procurement prerequisites — requiring a subsequent SOC 2 engagement that could have been the initial priority.

How to Get SOC 2 Certified in Wilmington: Step-by-Step Process

Obtaining SOC 2 Certification in Wilmington requires a structured sequence of organizational and audit activities that culminate in the issuance of a formal attestation report by a licensed CPA firm. The process demands internal preparation, evidence collection discipline, control documentation formalization, and active engagement with the external auditor throughout the observation period. Organizations that approach the SOC 2 process with clear internal ownership, documented control environments, and well-organized evidence repositories consistently achieve more efficient and successful audit outcomes.

- Identify applicable Trust Services Criteria based on services provided and client security commitments

- Define the system boundary and prepare the system description covering infrastructure, data flows, and personnel

- Document existing policies, procedures, and control activities for all applicable TSC control domains

- Establish evidence collection procedures and assign internal ownership for each control area

- Engage a Licensed CPA Firm to conduct the SOC 2 audit and agree on scope, timeline, and report type

- Complete Stage 1 (readiness evaluation) with the auditor to identify documentation gaps before the observation period

- Execute the formal audit observation period (6–12 months for Type II) with continuous evidence collection

- Respond to auditor findings and nonconformity notifications with management responses and supporting documentation

- Review the draft attestation report with management and confirm accuracy of the system description and findings

- Receive the final SOC 2 attestation report and distribute to authorized report users under applicable non-disclosure terms

- Maintain control environment and evidence processes throughout the year to prepare for the annual renewal audit cycle

Organizations pursuing SOC 2 Certification in Wilmington benefit from conducting internal control documentation reviews before engaging the external auditor. This internal preparation involves mapping existing security controls against the applicable Trust Services Criteria, identifying controls that are operated but not formally documented, and addressing areas where control ownership has not been explicitly assigned. The goal of internal preparation is to ensure that the organization’s control environment is documented in a manner that supports efficient evidence collection during the formal audit engagement — not to perform a mock audit outside the scope of appropriate pre-audit activities.

Evidence collection processes are a critical internal preparation element. Organizations must establish procedures for generating, capturing, and retaining system-generated records, approval logs, configuration screenshots, training completion records, and change management documentation that auditors will request as evidence of control operation. For SOC 2 Type II engagements, evidence must be available across the full observation period — meaning evidence collection must begin at the start of the period, not retrospectively when audit fieldwork commences. Organizations that establish automated evidence collection through GRC tooling or SIEM platforms reduce manual evidence preparation burden during audit execution.

SOC 2 audit reports can only be issued by licensed CPA firms operating under AICPA attestation standards. Organizations in Wilmington should select an audit firm that demonstrates specific expertise in SOC 2 engagements, familiarity with the technology and financial services sectors prevalent in Delaware, and the capacity to manage audit timelines that align with the organization’s commercial reporting requirements. CertPro operates as a Licensed CPA Firm with an established SOC 2 audit methodology structured around the AICPA Trust Services Criteria, delivering attestation reports for Wilmington-based service organizations across multiple industry sectors.

- ✓Internal Preparation Before the SOC 2 Audit

- ✓Selecting a Licensed CPA Firm for SOC 2 Audit Services in Wilmington

SOC 2 Certification in Wilmington: Industry-Specific Applications

SOC 2 attestation is applied across a broad range of industry sectors operating in Wilmington and the greater Delaware region. While the Trust Services Criteria framework is consistent across all engagements, the specific controls evaluated, the evidence populations assessed, and the risk factors addressed vary significantly across industries. Understanding how SOC 2 compliance applies to specific sectors in Wilmington helps organizations contextualize audit requirements within their operational reality and prioritize control development accordingly.

SOC 2 for Technology and SaaS Providers in Wilmington

Technology and SaaS organizations in Wilmington that deliver cloud-based platforms to financial institutions, healthcare organizations, or enterprise clients represent the most common category of SOC 2 audit engagement. These organizations typically scope their SOC 2 audit to cover Security and Availability criteria at minimum, with Confidentiality and Processing Integrity criteria added based on the specific data handling obligations embedded in their client service agreements. The system description for a SaaS provider includes the cloud infrastructure, application layer, data storage and transmission architecture, and the personnel and operational processes that govern system operation.

SOC 2 audit procedures for SaaS organizations evaluate specific technical controls including automated access provisioning and deprovisioning workflows, encryption key management processes, software development lifecycle security controls (SDLC security), penetration testing programs, infrastructure-as-code security review procedures, and container or cloud-native security configurations. Organizations that deploy on major cloud platforms — AWS, Microsoft Azure, or Google Cloud — can leverage their cloud provider’s existing SOC 2 and SOC 3 reports to address infrastructure-layer control requirements. This reduces the scope of controls that must be independently tested within the SaaS organization’s own audit.

SOC 2 for Healthcare Technology Organizations in Wilmington

Healthcare technology organizations operating in Wilmington — including electronic health record platforms, health data analytics companies, and patient-facing digital health applications — frequently pursue SOC 2 certification in conjunction with HIPAA compliance programs. While SOC 2 and HIPAA address distinct compliance obligations, the control frameworks are substantially overlapping. SOC 2’s Security criterion covers access control, encryption, monitoring, and incident response requirements that align directly with HIPAA Security Rule administrative, physical, and technical safeguard requirements. A well-scoped SOC 2 engagement produces audit evidence directly relevant to demonstrating HIPAA compliance during regulatory examinations.

SOC 2 for Managed Service Providers in Delaware

Managed service providers (MSPs) operating in Wilmington and the surrounding Delaware region that deliver IT infrastructure management, network security services, or cloud operations support to financial institutions and regulated entities must address the unique SOC 2 requirements that arise from their operational model. MSPs typically hold privileged administrative access to client systems, creating elevated security risk that auditors evaluate through specific controls around privileged access management, remote access security, client environment segregation, and security monitoring coverage across managed client environments.

Maintaining SOC 2 Compliance: Annual Audit Cycles and Continuous Control Monitoring

SOC 2 compliance is not a one-time achievement but an ongoing operational discipline requiring annual audit cycles and continuous control monitoring. Organizations that obtain SOC 2 Type II certification must repeat the audit process annually to maintain a current attestation report. Enterprise clients, regulated financial institutions, and third-party risk management programs in Wilmington require current reports — typically issued within the past twelve months — as evidence of ongoing compliance. Reports older than twelve months are generally considered stale and may be insufficient for vendor qualification purposes.

Continuous Control Monitoring Between Audit Cycles

Between formal audit engagements, organizations must maintain the control activities, evidence collection processes, and documentation update cycles established during the initial SOC 2 audit. Control failures or deviations that occur between audit cycles must be identified, documented, and remediated — and evidence of remediation must be preserved for evaluation in the subsequent audit period. Organizations that allow control discipline to lapse between audits frequently encounter elevated exception counts in their next Type II report, which can affect the audit opinion and the report’s usability in client due diligence processes.

Effective continuous control monitoring for Wilmington organizations involves establishing automated alerting for access control exceptions, change management deviations, and security monitoring gaps. It also requires maintaining policy review schedules that keep documentation current, conducting periodic internal control reviews between annual audit cycles, and tracking remediation timelines for control deficiencies identified in prior audit reports. Organizations that build continuous monitoring into their operational workflows produce cleaner evidence records and more efficient annual SOC 2 audit engagements.

Managing Scope Changes and Control Environment Evolution

Organizations in Wilmington that experience significant operational changes during a SOC 2 observation period — including new service launches, technology migrations, acquisition integrations, or major personnel changes — must assess the impact of those changes on the audit scope and communicate material changes to their auditor promptly. Changes that affect the system description, the control environment, or the population of systems within audit scope may require adjustments to the audit program and may affect the period covered by the final attestation report. Proactive communication with the auditor throughout the observation period reduces the risk of scope discrepancies that could delay report issuance.

Why Choose CertPro for SOC 2 Audit Services in Wilmington

CertPro operates as a Licensed CPA Firm conducting SOC 2 audit engagements under AICPA attestation standards for service organizations operating in Wilmington and across the United States. SOC 2 audit services for Wilmington, Delaware organizations conducted by CertPro are structured around a defined audit methodology that incorporates scope definition, audit program development, control testing, nonconformity review, and formal attestation report issuance in accordance with AT-C Section 205 requirements. CertPro’s audit professionals hold relevant credentials and maintain current knowledge of the AICPA Trust Services Criteria and applicable attestation guidance.

CertPro’s SOC 2 Audit Methodology

CertPro’s SOC 2 audit methodology is structured to deliver thorough, evidence-based evaluations that produce attestation reports meeting the assurance requirements of enterprise clients, regulated financial institutions, and third-party risk management programs in Wilmington. The methodology applies a risk-based approach to control testing, prioritizing higher-risk control areas while maintaining comprehensive coverage across all applicable Trust Services Criteria. Audit procedures are calibrated to the specific system under review, ensuring that testing activities reflect the actual operational characteristics of the organization’s environment rather than a generic control checklist.

For Wilmington organizations pursuing SOC 2 Type II certification, CertPro structures each audit engagement to accommodate the organization’s operational timeline, report distribution requirements, and client-facing reporting deadlines. Audit fieldwork is conducted efficiently using defined evidence request protocols that minimize disruption to the organization’s operational teams. Draft reports are reviewed with management before finalization to ensure accuracy of the system description and provide management with the opportunity to respond to identified control exceptions within the report documentation.

CertPro’s Experience with Wilmington Financial Services and Technology Sectors

CertPro’s SOC 2 audit practice includes specific experience with the control environments characteristic of Wilmington’s financial services technology sector — including payment processing platforms, credit risk analytics organizations, banking technology providers, and financial data management companies. This sector-specific familiarity enables CertPro auditors to apply relevant risk context to control evaluation procedures, identify control considerations specific to financial data processing environments, and produce attestation reports that address the assurance expectations of Wilmington’s institutional financial services clients.

- ✓Licensed CPA Firm issuing SOC 2 attestation reports under AICPA AT-C Section 205 standards

- ✓Structured audit methodology covering all five Trust Services Criteria categories

- ✓Experience with SOC 2 engagements across financial services, fintech, SaaS, and healthcare technology sectors

- ✓Defined evidence request protocols that minimize operational disruption during audit fieldwork

- ✓Risk-based testing approach calibrated to the specific control environment of each organization

- ✓Management review process for draft reports ensuring accuracy before final issuance

- ✓Annual audit cycle support for organizations maintaining current Type II certification status

- ✓Coordination of subservice organization reporting requirements for complex organizational structures

- ✓Transparent audit scope and timeline definition before engagement commencement

FAQ

▶

What is SOC 2 Certification and why is it important for Wilmington businesses?

▶

How long does a SOC 2 audit take for a Wilmington organization?

▶

Is SOC 2 certification mandatory for Wilmington financial technology companies?

▶

What is the difference between SOC 2 certified and SOC 2 compliant?

▶

How frequently must Wilmington organizations renew their SOC 2 certification?

▶

Which Trust Services Criteria should a Wilmington financial services technology company include?

▶

Can a SOC 2 report replace the need to complete vendor security questionnaires?

▶

How does SOC 2 attestation differ from SOC 1 and SOC 3 reports?

SOC 1 VS SOC 2: WHICH REPORT YOUR CUSTOMERS ACTUALLY ASK FOR

If you sell SaaS or provide outsourced services, you have likely been asked for a SOC report. However, the follow-up question is rarely easy to answer…

Secure Email Platform Exclaimer Renews ISO, SOC 2

Excerpt from The Manila Times Article, Published on February 26, 2026 Secure email solutions provider Exclaimer has renewed its ISO and SOC 2 certific…

SOC 2 FRAMEWORK REQUIREMENTS IN 2026. WHAT HAS CHANGED?

Security reviews used to happen at the tail end of a deal. Today, they happen in the first conversation. Enterprise buyers come prepared. They ask abo…

Get In Touch

have a question? let us get back to you.